Banks turn cautious on student loans as NPA's rise amid COVID-19 pandemic

With unemployment rising, the ability of those who have taken education loans to pay back has come down sharply. As a result, the non-performing assets (NPAs) have increased in the last one-and-a-half years.

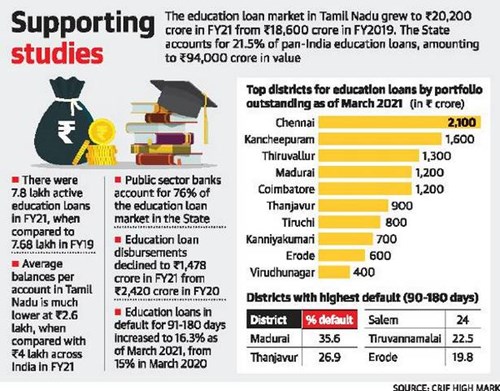

R. Nagarajan had taken a loan for his engineering course and started repaying it when he got a job at a start-up in the second half of 2019. In a few months, COVID-19 broke out and the start-up closed, leaving him and seven of his colleagues jobless. “I have not been able to repay the loan for over a year. And now I have a job with a lesser salary, and will have to close the loan soon,” he said. With the NPAs rising due to COVID-19, banks are very cautious.According to data from CRIF High Mark Credit Information Services, the education loan market in Tamil Nadu grew to ₹20,200 crore in March 2021 from ₹18,600 crore in March 2019. The data also showed that NPAs, measured in terms of portfolio at risk (PAR) for 91-180 days, increased to 16.3% as of March 2021 from 15% at the end of March 2020. PAR is the proportion of loans overdue (for a specific number of days) to the overall loans outstanding.

A senior official of the Chennai-based Indian Bank confirmed that the number of NPAs in the education loan sector had increased substantially, compared with the pre-pandemic period, and attributed the increase to unemployment and under-employment. For Indian Bank alone, the NPAs increased about 17.2% to ₹1,197.51 crore as on June 2021 from ₹1,021.1 crore as on September 2020.Even those who are seeking fresh education loans are finding it tough to get sanction. Parents of many students whom The Hindu spoke to said that after COVID-19 broke out, banks were reluctant to sanction loans, and some lamented that their reduced salaries did not meet the banks’ requirements. Data show that education loan disbursements declined to ₹1,478 crore in FY21 from ₹2,420 crore in FY20. But bankers say disbursements were low for several other reasons.

Reduction in demand

The Indian Bank official pointed out that there was a reduction in the demand mainly due to the decline in the demand in the recent years for engineering education, which constitutes a major exposure of loans under ₹7.50 lakh. Generally, engineering, medical and management courses account for a major portion of the demand for loans. He said the bank had not turned cautious in lending, since loans up to ₹7.50 lakh were covered under a credit guarantee scheme. “Tamil Nadu is an important region for education loans as the State accounts for one-third of the total number disbursed in the country,” said Vipul Jain, Head of Products, at CRIF High Mark. Under the Central Sector Interest Subsidy Scheme, full interest subsidy is provided for the moratorium period (the course period plus one year) on loans of up to ₹7.5 lakh taken from scheduled banks. The benefits are applicable to students of the weaker sections with a parental income of up to ₹4.5 lakh a year.

Some experts pointed out that political parties promising education loan waivers is also affecting repayment and the CIBIL score of students (the score is a measure of credit worthiness). The education loan waiver is one of the promises of the DMK as well as the AIADMK for the 2021 Assembly election

Source: Publication: Thehindu,19th July,2021