Microfinance Asset Quality Worsened in September on Lower Collections: CRIF

Microlenders have seen their asset quality worsen over the past year on lower repayment and collection levels during the pandemic.

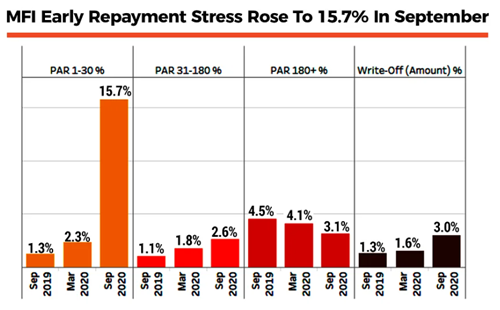

The early delinquency rate—portfolio at risk for 30 days past due—rose to 15.7% as of September 2020, according to a report by credit information agency CRIF High Mark. That compares with 2.3% in the preceding quarter and 1.3% a year earlier.

• The portfolio at risk for 31-180 days past due rose by 1.2 percentage points sequentially in July-September to 2.6%.

• Loans due for more than 180 days fell 1 percentage point sequentially to 3.1%.

• The loan writeoff amount nearly doubled to 3% in September compared with 1.6% as of March.

“In the quarter ended Sep. 30, delinquency levels for lenders in the microfinance space have risen quite sharply. This is an aberrant, short-term phenomenon," Alok Prasad, former chief executive of Microfinance Institutions Network, said. "Collection efficiencies have been improving over the past few months and should, broadly, reach normal levels by the end of this fiscal. However, from a forward looking perspective, the industry has to be ready for a significant level of writeoffs, say in the 5-10% range.” Among the top ten states for microfinance, West Bengal fared the worst as early repayment stress spiked to 31.72%, followed by Assam with 27.3% loans due past 30 days as of September. In the immediate aftermath of the six-month moratorium period declared by Reserve bank of India even as normalcy in business operations ensued, microfinance borrowers impacted severely due to the lockdown were not able to repay their dues, the report said. That led to "phenomenally high early delinquency value".

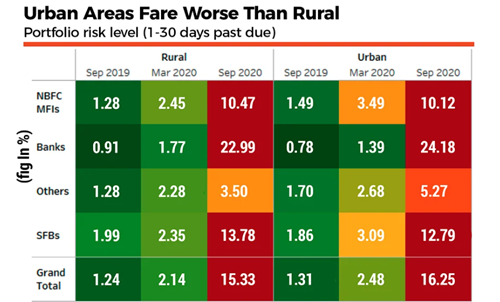

The early delinquency level for microlenders, however, was lower than the 24% portfolio at risk level (1-30 days past due) in urban areas for banks, while non-banking financial companies saw their stress levels rise to 10.12% and small finance banks witnessed a delinquency rate of 12.79% in the urban areas, the report said. On an overall basis, urban areas fared worse with a delinquency of 16.25% compared with 15.33% in rural areas. “The Covid-19 pandemic deeply impacted microfinance borrowers, particularly in the urban areas," Prasad. "This, as micro-enterprises got shut down and many clients returned to their villages due the disruptions and lockdown curbs."

The livelihoods of microfinance borrowers have suffered the most due to the pandemic as they are usually self-employed or own small businesses, leading to a sharp rise in delinquencies for microlenders, he said. “The debt moratorium also affected the repayment discipline of the borrowers. For many of them, repayment of past dues will be a challenge even as they pay the current instalments.” In September, an RBI paper had cautioned that the coronavirus pandemic could prove to be “the biggest tail risk event for the microfinance sector in a long time". This, the paper said, was mainly because a large chunk of microfinance borrowers are made up of small traders, hawkers and daily wage labourers—some of the worst hit employment categories amidst the pandemic. In September, the gross loan portfolio of microlenders fell 1.15% sequentially to Rs 224 crore, while disbursements grew nearly fourfold to Rs 29.7 crore in the July-September quarter, according to the report. As lending operations resumed after the lockdown, loans of higher ticket sizes (above Rs 40,000) showed a 10% rise in disbursements over the previous quarter, it said.

“Derailed by the Covid-19 pandemic, the microfinance sector is slowly and steadily returning to its tracks with a spike in fresh disbursements.," the report said. "However, since the pandemic is anything but over, repayments and collections still remain a concern for the sector, more so as the collection mechanism still continues to be physical and reach based, rather than digital.”

Source: Publication: bloombergquint , 07 Jan ,2021