Interest waiver: Lenders, credit bureaus race against time to identify borrowers

Home and property loans largest in terms of value; consumer, personal loans by number

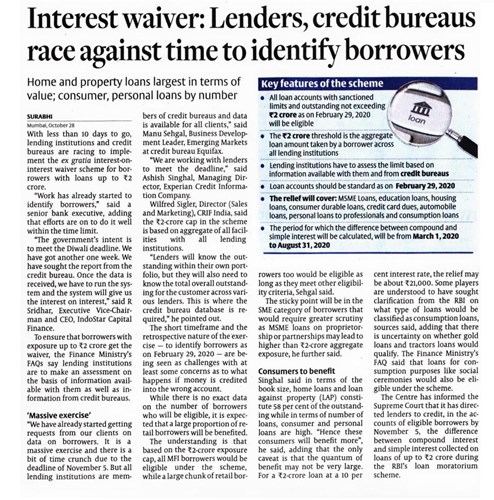

With less than 10 days to go, lending institutions and credit bureaus are racing to implement the ex gratia interest-on-interest waiver scheme for borrowers with loans up to ₹2 crore. “Work has already started to identify borrowers,” said a senior bank executive, adding that efforts are on to do it well within the time limit. “The government’s intent is to meet the Diwali deadline. We have got another one week. We have sought the report from the credit bureau. Once the data is received, we have to run the system and the system will give us the interest on interest,” said R Sridhar, Executive Vice-Chairman and CEO, IndoStar Capital Finance. To ensure that borrowers with exposure up to ₹2 crore get the waiver, the Finance Ministry’s FAQs say lending institutions are to make an assessment on the basis of information available with them as well as information from credit bureaus.

‘Massive exercise’

“We have already started getting requests from our clients on data on borrowers. It is a massive exercise and there is a bit of time crunch due to the deadline of November 5. But all lending institutions are members of credit bureaus and data is available for all clients,” said Manu Sehgal, Business Development Leader, Emerging Markets at credit bureau Equifax. “We are working with lenders to meet the deadline,” said Ashish Singhal, Managing Director, Experian Credit Information Company. Wilfred Sigler, Director (Sales and Marketing), CRIF India, said the ₹2-crore cap in the scheme is based on aggregate of all facilities with all lending institutions.

“Lenders will know the outstanding within their own portfolio, but they will also need to know the total overall outstanding for the customer across various lenders. This is where the credit bureau database is required,” he pointed out. The short timeframe and the retrospective nature of the exercise — to identify borrowers as on February 29, 2020 — are being seen as challenges with at least some concerns as to what happens if money is credited into the wrong account. While there is no exact data on the number of borrowers who will be eligible, it is expected that a large proportion of retail borrowers will be benefited. The understanding is that based on the ₹2-crore exposure cap, all MFI borrowers would be eligible under the scheme, while a large chunk of retail borrowers too would be eligible as long as they meet other eligibility criteria, Sehgal said. The sticky point will be in the SME category of borrowers that would require greater scrutiny as MSME loans on proprietorship or partnerships may lead to higher than ₹2-crore aggregate exposure, he further said.

Consumers to benefit

Singhal said in terms of the book size, home loans and loan against property (LAP) constitute 58 per cent of the outstanding while in terms of number of loans, consumer and personal loans are high. “Hence these consumers will benefit more”, he said, adding that the only caveat is that the quantum of benefit may not be very large. For a ₹2-crore loan at a 10 per cent interest rate, the relief may be about ₹21,000. Some players are understood to have sought clarification from the RBI on what type of loans would be classified as consumption loans, sources said, adding that there is uncertainty on whether gold loans and tractors loans would qualify. The Finance Ministry’s FAQ said that loans for consumption purposes like social ceremonies would also be eligible under the scheme.

The Centre has informed the Supreme Court that it has directed lenders to credit, in the accounts of eligible borrowers by November 5, the difference between compound interest and simple interest collected on loans of up to ₹2 crore during the RBI’s loan moratorium scheme.

Source: Publication: thehindubusinessline ,28th Oct,2020