A Deceptive Recovery

Collections by micro-finance institutions have rebounded in a big way, but delinquencies could surge, reports

Collections by microfinance institutions have rebounded in a big way, but delinquencies could surge.Micro-finance institutions (MFIS) have something to cheer about: collections are back to 85 per cent of the pre-covid lockdown levels. Yet Manoj Nambiar, managing director of Arohan Financial Services and chairman of the Microfinance Institutions Network, is not enthused: “The nature of this business is such that collections have to be closer to the 100 per cent mark.” On expected delinquencies after the loan moratorium ends today, he says “nobody has an idea on that front.”

What explains the rebound in collections? “The resilience of borrowers is remarkable. A vast majority of borrowers are in the essential services’ supply chain with tiny and micro businesses, and this has sprung back,” notes Udaya Kumar, managing director and chief executive officer (MD & CEO) at Credit access Grameen.

In the numbers

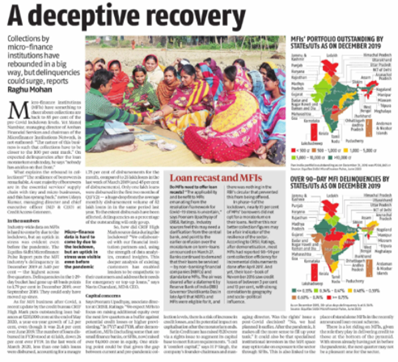

Industry-wide data on MFIS is hard to come by due to the lockdown, but an uptick in stress was evident even before the pandemic. The Equifax-sidbi Microfinance Pulse Report puts the MFI industry’s delinquency in December 2019 at 3.40 per cent — the highest across five quarters. Delinquencies in the 1-29day bucket had gone up 48 basis points to 1.79 per cent in December 2019, over September 2019. They could only have moved up since.

As for MFI business after Covid, a recent update by the credit bureau CRIF High Mark puts outstanding loan balances at ~235,000 crore at the end of May 2020, a year-on-year growth of 1.2 per cent, even though it was 21.4 per cent over June 2019. The number of loans disbursed in FY20 stood at 41 lakh, down 26 per cent over FY19. In the last week of March 2020, less than one lakh loans were disbursed, accounting for a meagre 1.75 per cent of disbursements for the month, compared to 25 lakh loans in the last week of March 2019 (and 45 per cent of disbursements). Only one lakh loans were disbursed in the first two months of Q1FY21 — a huge drop from the average monthly disbursement volume of 52 lakh loans in in the same period last year. To the extent disbursals have been affected, delinquencies as a percentage of the outstanding will only go up.

So, how did CRIF High Mark source data during the lockdown? “We collaborated with our financial institution partners and, using the strength of data analytics, created insights. This deeper analysis of existing customers has enabled lenders to be empathetic to their customers and address their needs for emergency or top-up loans,” says Navin Chandani, MD & CEO.

Micro-finance data is hard to come by due to the lockdown, but an uptick in stress was visible even before the pandemic.

Capital concerns

Says Poonam Upadhyay, associate director at CRISIL Ratings: “We expect MFIS to focus on raising additional equity over the next few quarters as a buffer against potential credit losses or higher provisioning.” In FY17 and FY18, after demonetisation, MFIS (including some that are small finance banks, or SFBS, now) raised over ~4,000 crore in equity. One sticking point could be that given the gap between current and pre-pandemic collection levels, there is a risk of increase in credit losses, and its potential impact on capitalisation after the moratorium ends.

Satin Credit care has raised ~120 crore via a rights issue to augment its capital base to meet future requirements. “I call it ‘comfort capital’,” says H P Singh, the company’s founder-chairman and managing director. Was the rights’ issue a post-covid decision? “No, we had planned it earlier. After the pandemic, it makes all the more sense to fill up your tank.” It could also be that specialised institutional investors in the MFI space may opt to take on exposure to the sector through SFBS. This is also linked to the place of standalone MFIS in the recently announced loan-recast scheme.

There is a lot riding on MFIS, given the role they play in delivering credit to those at the bottom of the pyramid. With stress already having set in before the pandemic, the next quarter may not be a pleasant one for the sector.

Source: Publication: Business-Standard ,31st August 2020