Covid-19: Retail lending may not remain steady source of business for banks

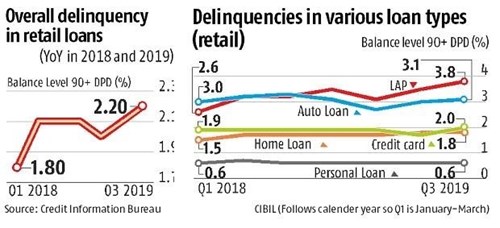

With a demand destruction, following the coronavirus (Covid-19)-driven lockdown, retail lending may no more be a steady source of business and revenue for banks, at least in the current financial year (FY21). Delinquencies in unsecured loans are already on the rise. Now, other segments of retail loans — auto and consumer durables — may witness an upward trajectory in defaults.

Senior bank executives said with little or no investment demand from the corporate sector for the last many quarters, banks and NBFCs have been focusing on the retail segment — individual and households — to hawk consumer durables credit as well as housing and personal loans. The first cut assessment indicates shock from the coronavirus outbreak is going to be much severe with a scale much higher than the global financial crisis in 2007-2008. Delinquencies could also be on the rise on the already stressed books, bankers said.

SBI executive said the bank had indicated an 18 per cent rate for expanding retail loan in FY21. But that was in February, before Covid-19 hit the world. The target would certainly be revised downwards when the bank gets back to the drawing board to assess business prospects in the changed environment. Its retail loan book grew 17.5 per cent year-on-year (YoY) to Rs 7.19 trillion till the end of December 2019.

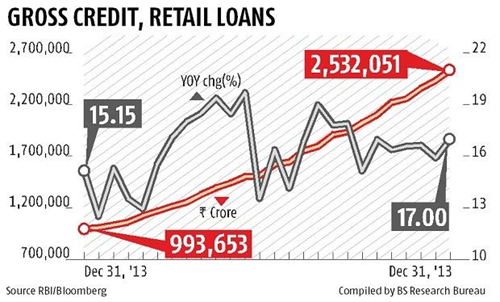

At present, the focus is on supporting bank staff and meeting their needs when the working and commuting to branches has become a challenge now, said the SBI executive. The retail loan business of banks in segments like home loans and credit cards has expanded at a steady pace of over 15 per cent YoY for over two-and-a-half years. This contrasts with the dip in economic growth. The segment clocked 17 per cent growth (YoY) in February 2020, according to Reserve Bank of India (RI) data.

Prakash Agarwal, director and head of financial institutions, India Ratings, said the retail segment was giving substantial revenue to banks. Now, with disruption due to the Covid-driven lockdown, this revenue stream will also come under pressure.The RBI has permitted a three-month moratorium (March-May 2020) on payment of loans as an initial step to support those hit by the crisis. The picture is still evolving and further extension (of moratorium) will depend on severity of challenges, said Agarwal.

The expansion in retail segment will be hit badly as the Indian economy may contract or post a very small growth. The effects may not be visible immediately but would be known in the coming quarters as it happened in the case of demonetisation.

Navin Chandani, chief executive officer (CEO), CRIF High Mark, a credit information bureau, said there will be a constructive fallout from the current situation for digital banking. Banks and finance companies may do more lending business in the retail segment on the digital platform – KYC (know your customer protocol) and underwriting. The lending strategy will be fine-tuned for specific segments, keeping in mind risks and policies, he added.

Source: Publication: Business Standard | 9th April 2020