No End to NBFC Credit Slide Show

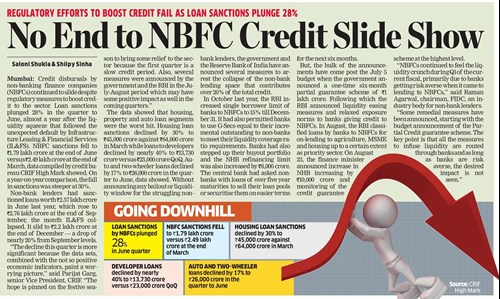

Credit disbursals by non-banking finance companies (NBFCs) continued to slide despite regulatory measures to boost credit to the sector. Loan sanctions plunged 28% in the quarter to June, almost a year after the liquidity squeeze that followed the unexpected default by Infrastructure Leasing & Financial Services (IL&FS). NBFC sanctions fell to ₹1.79 lakh crore at the end of June versus ₹2.49 lakh crore at the end of March, data compiled by credit bureau CRIF High Mark showed. On a year-on-year comparison, the fall in sanctions was steeper at 30%. Non-bank lenders had sanctioned loans worth ₹2.57 lakh crore in June last year, which rose to ₹2.76 lakh crore at the end of September, the month IL&FS collapsed. It slid to ₹2.2 lakh crore at the end of December — a drop of nearly 20% from September levels.

“The decline this quarter is more significant because the data sets, combined with the not so positive economic indicators, paint a worrying picture,” said Parijat Garg, senior Vice President, CRIF. “The hope is pinned on the festive season to bring some relief to the sector because the first quarter is a slow credit period. Also, several measures were announced by the government and the RBI in the July-August period which may have some positive impact as well in the coming quarters.”

The data showed that housing, property and auto loan segments were the worst hit. Housing loan sanctions declined by 30% to ₹45,000 crore against ₹64,000 crore in March while loans to developers declined by nearly 40% to ₹13,730 crore versus ₹23,000 crore QoQ. Auto and two-wheeler loans declined by 17% to ₹26,000 crore in the quarter to June, data showed. Without announcing any bailout or liquidity window for the struggling nonbank lenders, the government and the Reserve Bank of India have announced several measures to arrest the collapse of the non-bank lending space that contributes over 20% of the total credit.

In October last year, the RBI increased single borrower limit of banks to NBFCs to 15% till December 31. It had also permitted banks to use G-Secs equal to their incremental outstanding to non-banks to meet their liquidity coverage ratio requirements. Banks had also stepped up their buyout portfolio and the NHB refinancing limit was also increased by ₹6,000 crore. The central bank had asked nonbanks with loans of over five year maturities to sell their loan pools or securitise them on easier terms for the next six months.

But, the bulk of the announcements have come post the July 5 budget when the government announced a one-time six-month partial guarantee scheme of ₹1 lakh crore. Following which the RBI announced liquidity easing measures and relaxed exposure norms to banks giving credit to NBFCs. In August, the RBI classified loans by banks to NBFCs for on-lending to agriculture, MSME and housing up to a certain extent as priority sector. On August 23, the finance minister announced increase in NHB increasing by ₹10,000 crore and monitoring of the credit guarantee scheme at the highest level.

“NBFCs continued to feel the liquidity crunch during Q1of the current fiscal, primarily due to banks getting risk averse when it came to lending to NBFCs,” said Raman Agarwal, chairman, FIDC, an industry body for non-bank lenders.

“Some remedial measures have been announced, starting with the budget announcement of the Partial Credit guarantee scheme. The key point is that all the measures to infuse liquidity are routed through banks and as long as banks are risk averse, the desired impact is not seen.”

Source: Publication: The Economic Times, Delhi| Page No-10