Here’s Why You Must Avoid Rental Deposit Loans

There are personal loans available for a whole host of customer requirements. Now, Millennials and mid-age consumers take personal loan schemes despite high interest rates. There is now an increased preference for such loans as fintech companies too offer these products. The application process is quick and the loan gets sanctioned in one or two days.

One segment gaining popularity among salaried professionals is the loan for rental deposit. In fact, online lending company LoanTap has witnessed a growth of 45-50 per cent in rental deposit loans as of March 2019 compared to the figures reported a year ago.Before you decide to take the plunge into taking these loans, understand all aspects in detail and take an informed call.

What is a rental deposit loan?

Now, a tenant’s biggest worry is raising the amount needed for the security deposit while renting an apartment.Landlords in metropolitan cities ask for a deposit equivalent to six months to one year’s rent before letting their houses out. So, even as you move cities for better job opportunities, your savings take a knock while renting an apartment. Typically, a sum of Rs 1-3 lakh gets blocked in security deposits.

For example, let’s say you shift to Pune from Surat for a job and decide to rent a flat closer to office. If the rent is Rs 30,000 per month the rental deposit you need to pay your landlord will be Rs 1.8 lakh. Although this deposit gets refunded to you when you vacate the flat, it is a huge amount to arrange for you if you are just entering the workforce or even if you are in your second job. Now, fintech companies such as LoanTap, Paymatrix and Cashe and non-banking financial company (NBFC) Bajaj Finserv offer loans for rental deposit. There are mild variations in their product offerings, but the end-purpose is to lend for rental deposit.

How does the scheme work?

While borrowing from LoanTap or Paymatrix, the loan amount sanctioned is between Rs 1 lakh to Rs 5 lakh. An individual working for a public limited/private company or in a government job with monthly take home salary of more than Rs 30,000 is eligible for this loan. The tenure of this loan is 11-33 months—it should match the duration of the rental agreement. The interest rate charged per month is a flat 1.5 per cent (i.e., 18 per cent per annum).

Amit Tewary, Chief Operating Officer, LoanTap says, “You will only pay interest throughout the lease tenure and repay the principal amount upon termination of lease agreement. The principal amount is directly credited to the landlord’s bank account by the lender.” The repayment of the principal is done by the loan applicant, the tenant, at the end of the tenure. Another lender, Cashe, disburses a maximum loan up to Rs 2 lakh for rental deposit and the repayment tenure is a maximum of six months. The rate of interest is 2.5 per cent per month (i.e. 15 per cent for six months tenure loan). You need to repay principal and interest in six equated monthly instalments (EMIs).

Bajaj Finserv offers a rental deposit loan of up to Rs 5 lakh to the tenant. As a tenant, you can choose a tenor of up to 36 months to repay the loan. For instance, if Rs 3 lakh is sanctioned to you in rental deposit scheme, with the flexi hybrid facility, you can borrow Rs 50,000 in May 2019 from the sanctioned amount to pay the brokerage charges, and then borrow Rs 2 lakh in June 2019 to pay the deposit amount to the landlord. Lastly, you can borrow the remaining Rs 50,000 in July 2019 to pay advance rent. You need to pay interest only on the amount utilised from the sanctioned amount during the tenure of loan. Processing charges vary from lender to lender, and are usually in the range of 2-5 per cent.

What’s different about the scheme?

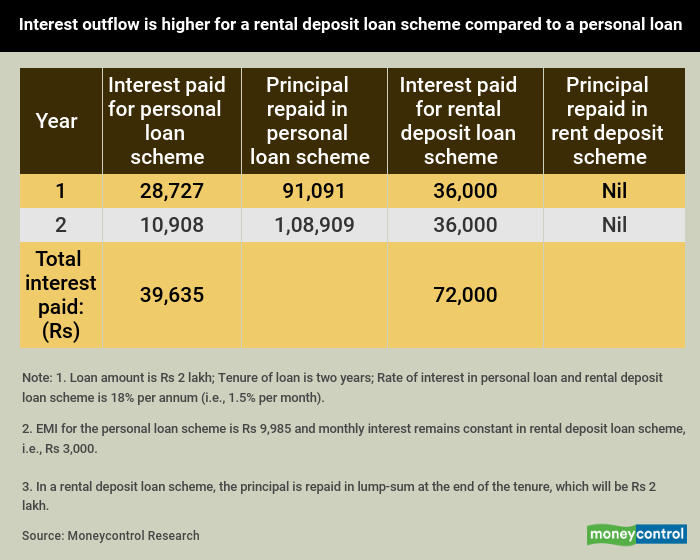

Throughout the tenure of the loan, if the interest is 1.5 per cent (flat interest rate), you will only pay Rs 1,500 per month for Rs 1 lakh. However, Parijat Garg, Senior Vice President at credit bureau CRIF cautions, “In rental deposit loans, though the monthly payout is lower, the overall interest outflow is higher because the borrower is only servicing the interest component at a flat rate. The principal amount stays constant and is repaid at the end of tenure as a bullet payment.” In a conventional personal loan scheme, the interest charge is on the reducing principal balance. So, you pay lower interest at the end of tenure compared to what you pay for a rental deposit loan.

There are no foreclosure charges after six months of the loan tenure. But, fintech companies such as LoanTap and Paymatrix are charge four per cent as foreclosing charges on the entire principal amount from the borrower if full repayment is done before six months. Garg says, “The foreclosure charges here may turn out be more compared to what is paid to foreclose a personal loan, since in the case of personal loans, 3-4 per cent charges are applied on the outstanding principal amount, which reduces with each EMI payment.”

Moneycontrol’s take

You would be better off avoiding the rental deposit loan scheme, as you will end up paying higher interest during the tenure of the loan as explained above. If you must take a loan to pay your rental deposit, a conventional personal loan works better. The rental deposit loan is useful for borrowers who cannot repay the higher EMIs that are charged in conventional personal loan schemes. However, it’s a bad idea to start your working career with loans, especially if you are still repaying your education loan.

Source: moneycontrol