Non-Bank Microfinance Companies Face Another Test On Loan Quality- CRIF Insights

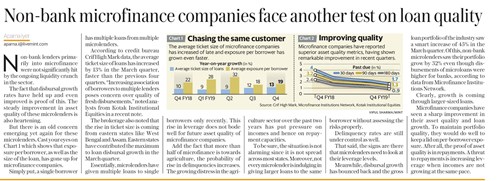

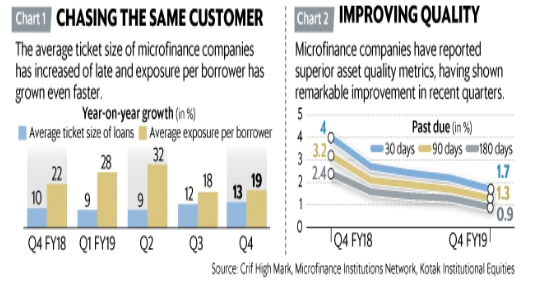

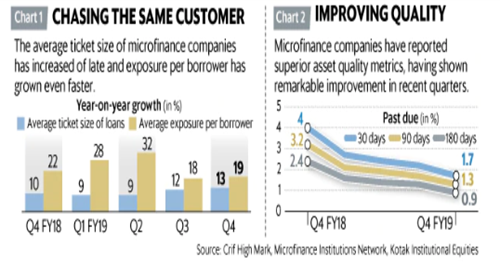

Non-bank lenders primarily into microfinance were not significantly hit by the ongoing liquidity crunch in the sector. The fact that disbursal growth rates have held up and even improved is proof of this. The steady improvement in asset quality of these microlenders is also heartening. But there is an old concern emerging yet again for these microlenders. Cast your eyes on Chart 1 which shows that exposure per borrower, as well as the size of the loan, has gone up for microfinance companies. Simply put, a single borrower has multiple loans from multiple microlenders.

According to credit bureau Crif High Mark data, the average ticket size of loans has increased by 13% in the March quarter, faster than the previous four quarters. “Increasing association of borrowers to multiple lenders poses concern over quality of fresh disbursements," noted analysts from Kotak Institutional Equities in a recent note. The brokerage also noted that the rise in ticket size is coming from eastern states like West Bengal and Assam. Eastern states have contributed the maximum to loan disbursal growth in the March quarter.

Essentially, microlenders have given multiple loans to single borrowers only recently. This rise in leverage does not bode well for future asset quality of microfinance companies. Add the fact that more than half of microfinance is towards agriculture, the probability of rise in delinquencies increases. The growing distress in the agriculture sector over the past two years has put pressure on incomes and hence on repayment capacities.

To be sure, the situation is not alarming since it is not spread across most states. Moreover, not every microlender is indulging in giving larger loans to the same borrower without assessing the risks properly. Delinquency rates are still under control as well. That said, the signs are there that microlenders need to look at their leverage levels.

Meanwhile, disbursal growth has bounced back and the gross loan portfolio of the industry saw a smart increase of 45% in the March quarter. Of this, non-bank microlenders saw their portfolio grow by 32% even though disbursements of microloans were higher for banks, according to data from Microfinance Institutions Network.Clearly, growth is coming through larger-sized loans.

Microfinance companies have seen a sharp improvement in their asset quality and loan growth. To maintain portfolio quality, they would do well to keep a lid on per-borrower exposure. After all, the proof of asset quality is in repayments. A threat to repayments is increasing leverage when incomes are not growing at the same pace.

Original Source: Publication: Livemint, Delhi| Page No-04