How Credit-Worthy Are You?

Here are a few metrics to help you understand, evaluate and improve your credit score

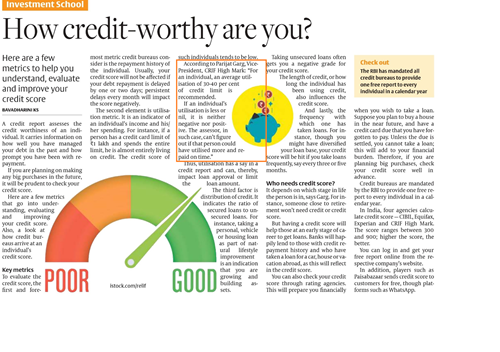

A credit report assesses the creditworthiness of an individual. It carries information on how well you have managed your debt in the past and how prompt you have been with repayment. If you are planning on making any big purchases in the future, it will be prudent to check your credit score.

Here are a few metrics that go into understanding, evaluating and improving your credit score. Also, a look at how credit bureaus arrive at an individual’s credit score.

Key metrics

To evaluate the credit score, the first and foremost metric credit bureaus consider is the repayment history of the individual. Usually, your credit score will not be affected if your debt repayment is delayed by one or two days; persistent delays every month will impact the score negatively.

The second element is utilization metric. It is an indicator of an individual’s income and his/her spending. For instance, if a person has a credit card limit of ₹1 lakh and spends the entire limit, he is almost entirely living on credit. The credit score of such individuals tends to be low.

According to Parijat Garg, Vice-President, CRIF High Mark: “For an individual, an average utilization of 30-40 percent of credit limit is recommended. If an individual’s utilization is less or nil, it is neither negative nor positive. The assessor, in such case, can’t figure out if that person could have utilized more and repaid on time.” Thus, utilization has a say in a credit report and can, thereby, impact loan approval or limit the loan amount.

The third factor is the distribution of credit. It indicates the ratio of secured loans to unsecured loans. For instance, taking a personal, vehicle or housing loan as part of natural lifestyle improvement is an indication that you are growing and building assets. Taking unsecured loans often gets you a negative grade for your credit score. The length of credit, or how long the individual has been using credit, also influences the credit score.

And lastly, the frequency with which one has taken loans. For instance, though you might have diversified your loan base, your credit score will be hit if you take loans frequently, say every three or five months.

Who needs a credit score?

It depends on which stage in life the person is in, says Garg. For instance, someone close to retirement won’t need credit or credit score. But having a credit score will help those at an early stage of career to get loans. Banks will happily lend to those with credit repayment history and who have taken a loan for a car, house or vacation abroad, as this will reflect in the credit score.

You can also check your credit score through rating agencies. This will prepare you financially when you wish to take a loan. Suppose you plan to buy a house in the near future and have a credit card due that you have forgotten to pay. Unless the due is settled, you cannot take a loan; this will add to your financial burden. Therefore, if you are planning big purchases, check your credit score well in advance.

Credit bureaus are mandated by the RBI to provide one free report to every individual in a calendar year. In India, four agencies calculate credit score — CIBIL, Equifax, Experian, and CRIF High Mark. The score ranges between 300 and 900; higher the score, the better. You can log in and get your free report online from the respective company’s website. In addition, players such as Paisabazaar sends credit score to customers for free, through platforms such as WhatsApp.

Print:

The Hindu Business Line | Page No 03 |Edition: Chennai