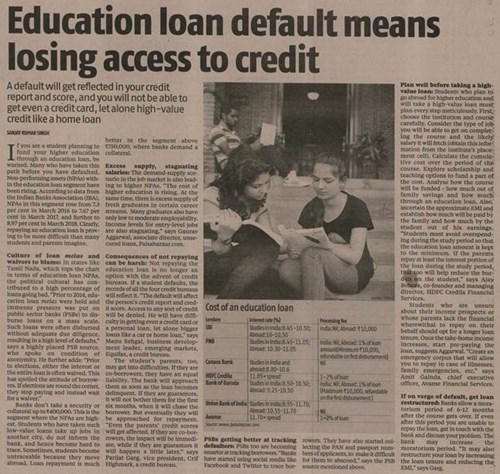

Be careful, students! Education loan default means losing access to credit- Parijat’s views on the Education loan with Business Standard

A default will get reflected in your credit report and score, and you will not be able to get even a credit card, let alone high-value credit like a home loan.

If you are a student planning to fund your higher education through an education loan, be warned. Many who have taken this path before you have defaulted. Non-performing assets (NPAs) within the education loan segment have been rising.

According to data from the Indian Banks Association (IBA), NPAs in this segment rose from 7.3 percent in March 2016 to 7.67 percent in March 2017, and further to 8.97 percent in March 2018. Clearly, repaying an education loan is proving to be more difficult than many students and parents imagine.

Consequences of not repaying the loan can be harsh! The student's parents too may get into difficulties. If they are co-borrowers, they have an equal liability." Even the parent's credit scores will get affected. If they are co-borrowers, the impact will be immediate, while if they are guarantors it will happen a little later," says Parijat Garg, Vice President, CRIF High Mark, a credit bureau.

If on verge of default, get loan restructured. Banks allow a moratorium period of 6-12 months after the course gets over." It may also restructure your loan by increasing the loan and reducing the EMI," says Garg.

To read the full coverage, click on the below picture.

Original Source: Business Standard- August 19, 2018, | Page No 12 |Edition: National