What Are The Five Cs Of Credit?

Short Answer - The five Cs of credit, Character, Capacity, Capital, Collateral, and Conditions, help lenders assess a borrower’s creditworthiness. They evaluate repayment history, income, investments, pledged assets, and external factors to determine risk, guiding loan approvals and ensuring responsible borrowing.

In the dynamic world of personal finance, availing of credit, whether it's a credit card or loan, can help you achieve your financial goals. However, when you approach any lender to avail of a loan or apply for a credit card, they may want to verify whether you have the financial capacity to repay the amount on time and in accordance with the agreed-upon terms and conditions.

Financial organisations assess your creditworthiness by reviewing your credit report and understanding your past debt management and repayment capacity. They achieve this by checking the 5 Cs of credit.

As a potential borrower, it is important that you have a good understanding of the 5 Cs of credit. It will help you navigate the credit landscape successfully and make more informed borrowing decisions.

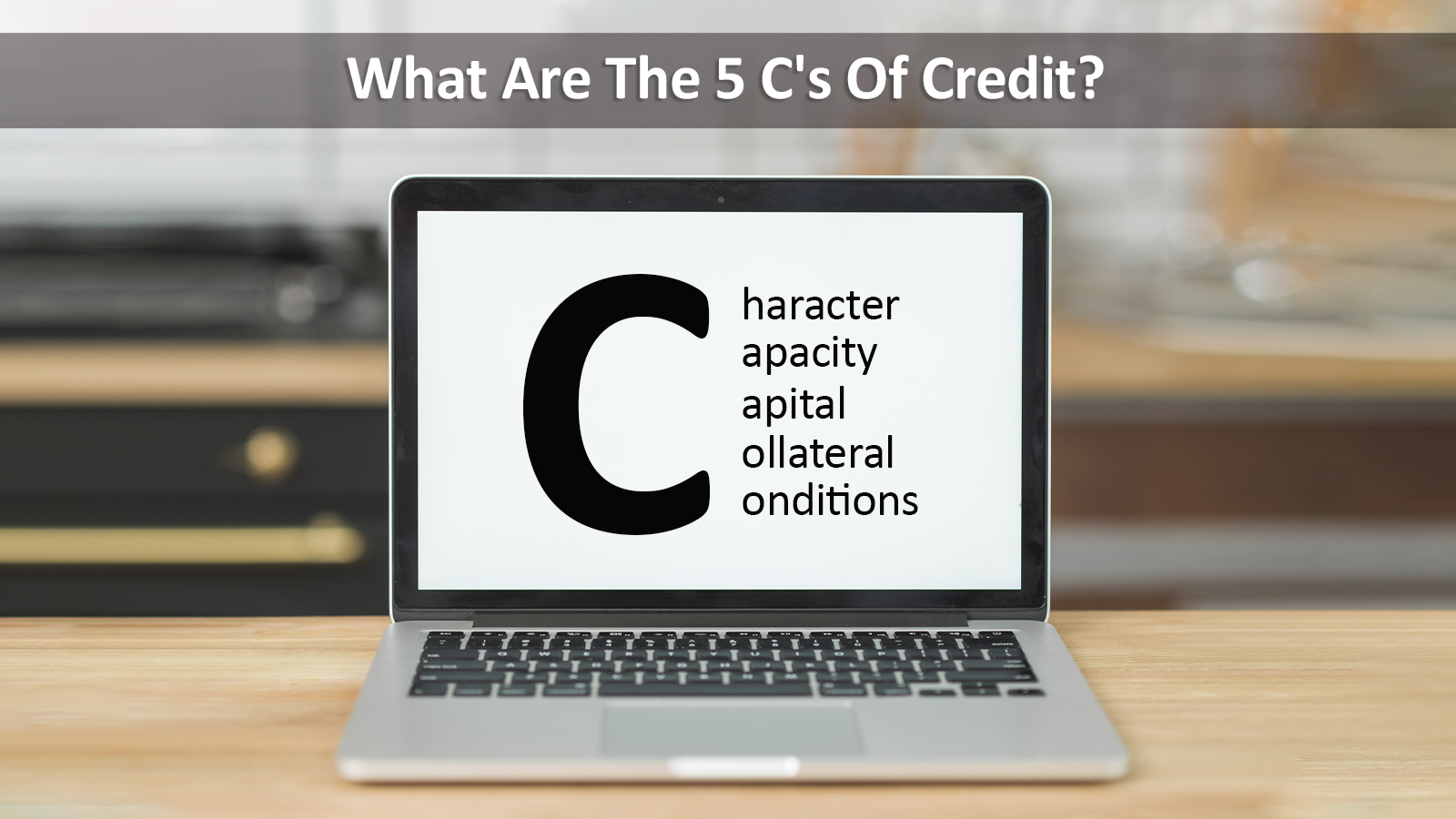

The 5 Cs of credit are – character, capacity, capital collateral, and conditions. Let's understand them in detail below.

Character

The first C in the credit evaluation process is character. This essentially refers to your credibility or reputation for repaying debts you incur and your overall credit history. When you apply for a loan, financial institutions scrutinise your credit report, which includes details about your personal credit score, repayment history, debts, and any missed or late payments.

As a potential loan applicant, it is paramount that you maintain a good credit score to showcase positive character to the lenders. Also, a high credit score will showcase that you are responsible with your finances, and you may have better chances of getting the loan approved with better terms and conditions to suit your requirements.

Capacity

The second C in the 5 Cs of credit is capacity. It basically represents your ability to repay the loan based on your income level, employment history and stability, and existing financial obligations. Before extending the loan to you, the lenders want to ensure that you have a steady income source and that you can afford the monthly payments while managing your regular expenses.

Before you submit your loan application, it is advisable that you carefully assess your financial condition and apply for a loan that you can easily afford to repay without compromising on your other financial goals.

Capital

One of the most critical aspects of the 5 c's of credit analysis is capital.

The amount of money the borrower has invested in their business or assets – their “skin in the game”. Capital is mainly assessed in terms of

- Net worth of the individual or business.

- Owner’s equity in the business.

- Down payment made in a loan (especially in project or asset-based finance).

Higher capital means the borrower is taking more risk personally, which reduces the lender’s risk.

Collateral

Collateral is a type of security that lenders may require to extend certain types of loans, especially for large-ticket items. It involves pledging an asset like gold, hypothecation of an asset like a vehicle, or mortgage of an asset such as a property against the amount you borrow. If you fail to repay the amount on time, the lender has the authority to take ownership of the asset to recover the amount.

While a personal loan typically does not require collateral, some lenders may request it, especially if you do not have a good credit history. Furthermore, when you offer collateral, it mitigates the risk for the lender, and you may get the loan with more favourable terms.

As a potential borrower, you must be careful about the implications of providing collateral, as it may put the asset at risk if you fail to repay the loan on time and as per the agreed loan terms and conditions.

Conclusion

In the 5 Cs of credit parlance, conditions refer to various external factors that may affect your ability to repay the amount you borrow. Financial organisations consider several factors like the purpose of the loan, your financial conditions, potential changes in the financial situation, business credit score (if you are a business owner/self-employed and applying for a business loan), etc. while assessing your eligibility.

.