Understanding the CRIF Company Credit Report with a Sample

Short Answer - loan performance, and risk indicators. Understanding each section helps businesses identify credit strengths, address issues, and improve loan eligibility by presenting a transparent and reliable credit profile to lenders.

A company credit report and credit score are core indicators of a business’s creditworthiness and play a critical role in determining loan eligibility. Lenders rely on these reports to assess repayment behaviour, financial discipline, and overall risk before approving business loans.

Among the credit information companies in India, CRIF High Mark provides detailed company credit reports that help both lenders and borrowers make informed decisions.

This guide explains what a CRIF company credit report contains and how to read and interpret each section effectively.

What Is a CRIF Company Credit Report?

A CRIF company credit report is a comprehensive record of a business’s credit history, borrowing behaviour, and financial relationships. It consolidates data submitted by banks and financial institutions to provide lenders with a clear picture of a company’s past and present credit exposure.

For businesses, the report serves as a valuable tool to understand how lenders view their credit profile and to identify areas that may need improvement before applying for financing.

What Information Does a CRIF Company Credit Report Contain?

A CRIF company credit report includes information about the following.

Business Information

This section includes basic details about the business, such as its nature of business, industry, registered address, contact information, and stakeholder details, including partners, promoters, or holding companies. It also provides a summary of credit facilities previously availed and their current status.

Business Credit Score

The business credit score (also called Business Credit Rank) reflects the company’s creditworthiness based on its repayment track record. Lenders use this score to evaluate risk and make faster credit decisions.

Loan History

Details of all credit facilities availed by the business(active and closed) are recorded here. This includes repayment history for the past 36 months and any credit facilities the business has guaranteed.

Past Searches

This section shows all inquiries made by lenders against the company and the number of credit facilities sought from new lenders over the past 24 months.

How to Read and Interpret Your CRIF Business Credit Report?

To interpret your CRIF company credit report correctly, it is important to understand the purpose of each section and how lenders analyse the information presented.

The following are the key sections of the report:

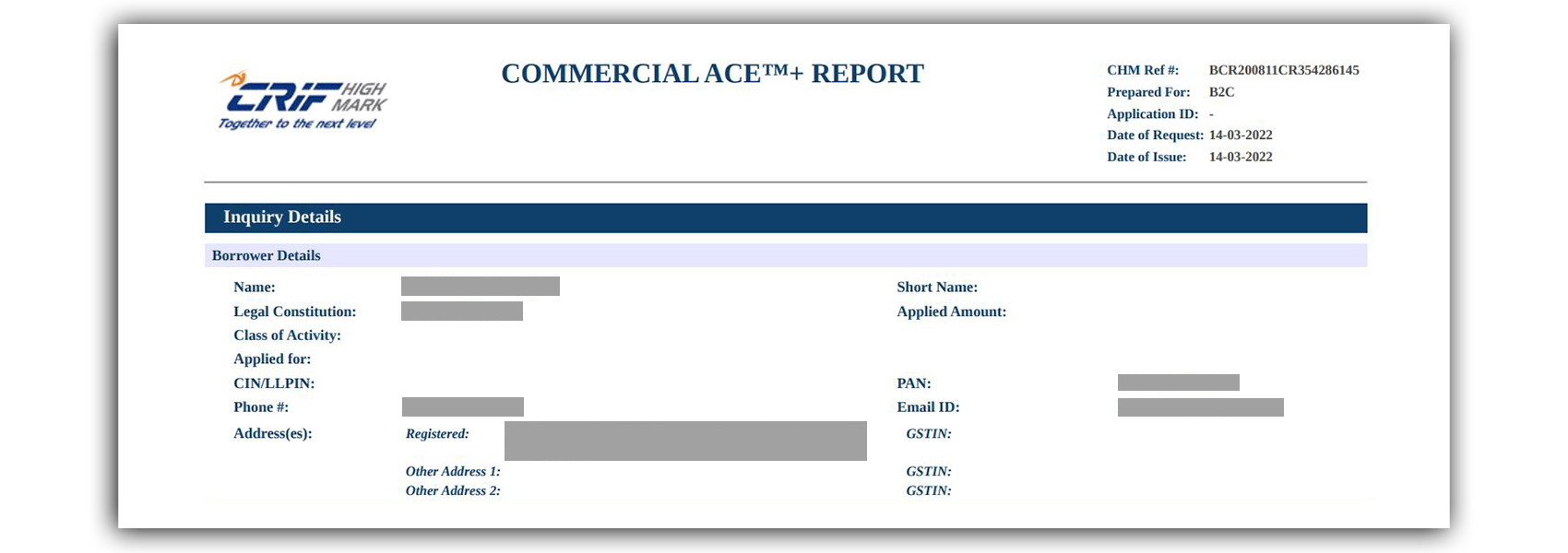

Inquiry Details

This section outlines borrower identification details such as the business name, legal constitution, class of activity, address, contact details, PAN, GSTIN, and CIN.

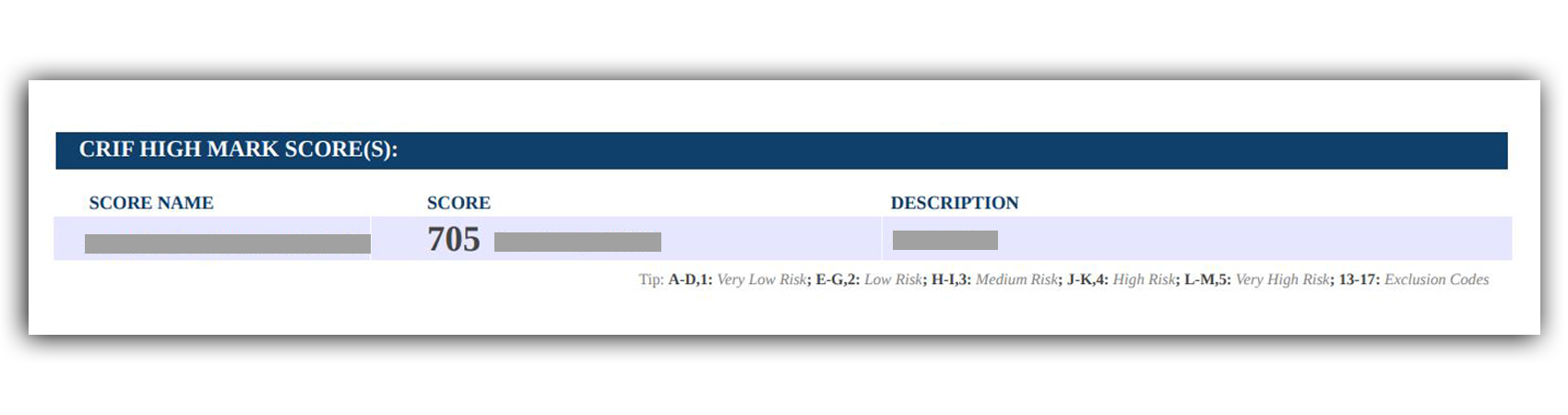

CRIF High Mark Score

This section highlights the company’s credit risk and the likelihood of loan approval. The score is presented either as a numeric range from 300 to 900 or as a rank from 1 to 5, depending on exposure and the number of tradelines.

Risk Classification Explained:

- A-D: Very Low Risk

- E-G: Low Risk

- H-I: Medium Risk

- J-K: High Risk

- L-M: Very High Risk

- 13-17: Exclusion Codes

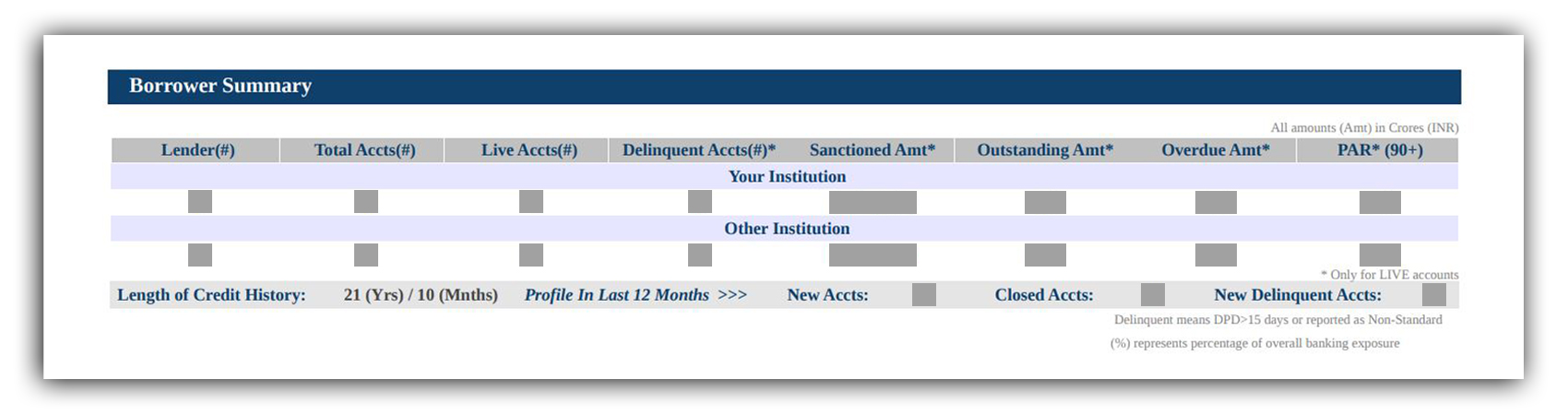

Borrower Summary

This section provides a snapshot of the company’s credit history, including the number of lenders, loan amounts, outstanding dues, and payment status over the last 12 months for both direct borrowings and guaranteed loans.

A delinquent account refers to a loan that has not been paid on time. PAR (Portfolio at Risk) represents the total outstanding amount of accounts with payments overdue by more than 90 days.

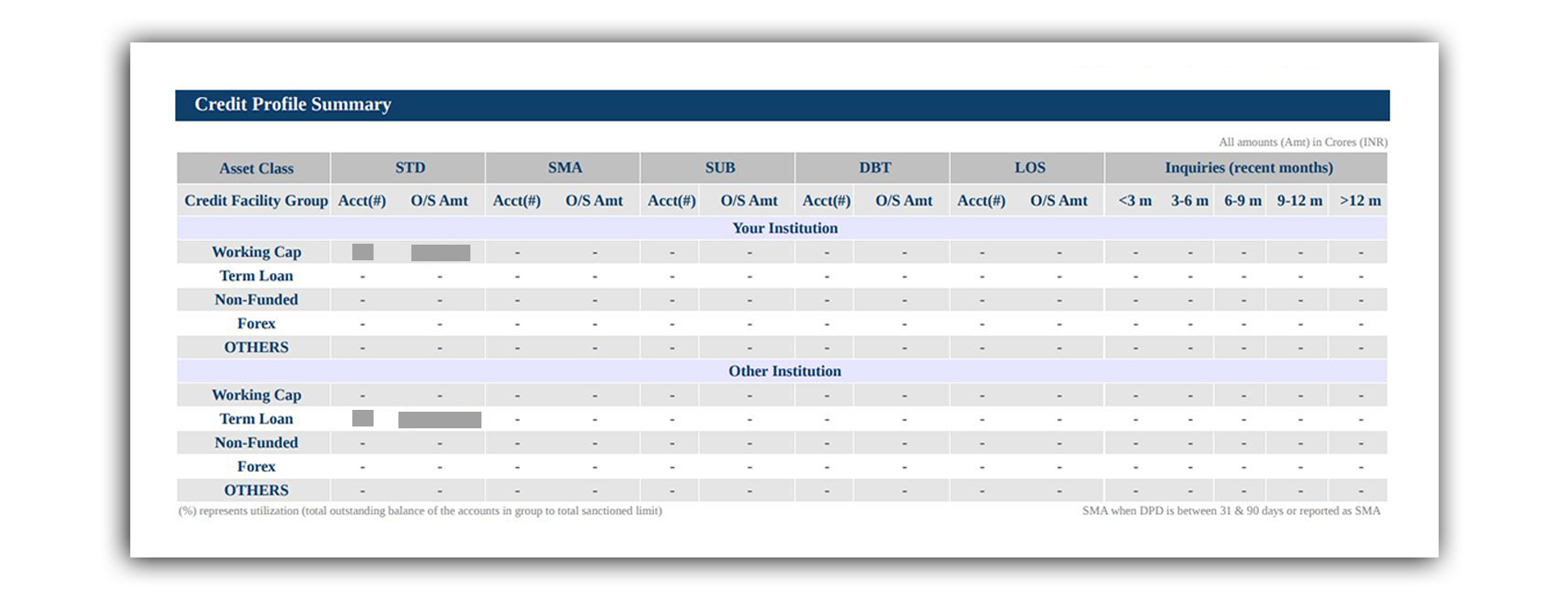

Credit Profile Summary

The credit profile summary outlines the types of loans availed, sanctioned amounts, total outstanding balances, credit utilisation levels, and recent credit inquiries related to the business and its guarantees.

Additional Status

This section highlights any derogatory information reported in the last two years, such as willful defaults, write-offs, suits filed, restructured credit facilities, or invoked guarantees. Lenders closely examine this section as it significantly impacts loan approval decisions.

New Credit Facilities

Any new credit facility, such as working capital loans, term loans, or forex facilities, availed in the past 12 months, appears in this section.

Top 5 Non-Standard Credit Facilities (Reported for 24 Months

This section lists non-standard credit facilities availed in the last 24 months. It includes details such as the lender’s name, type of facility, sanction amount, sanction date, outstanding balance, and overdue amount.

Firmographic Data

This data provides company-level information sourced from the Ministry of Corporate Affairs (MCA), including key company details and the charges index, helping lenders gain deeper insights into the business structure.

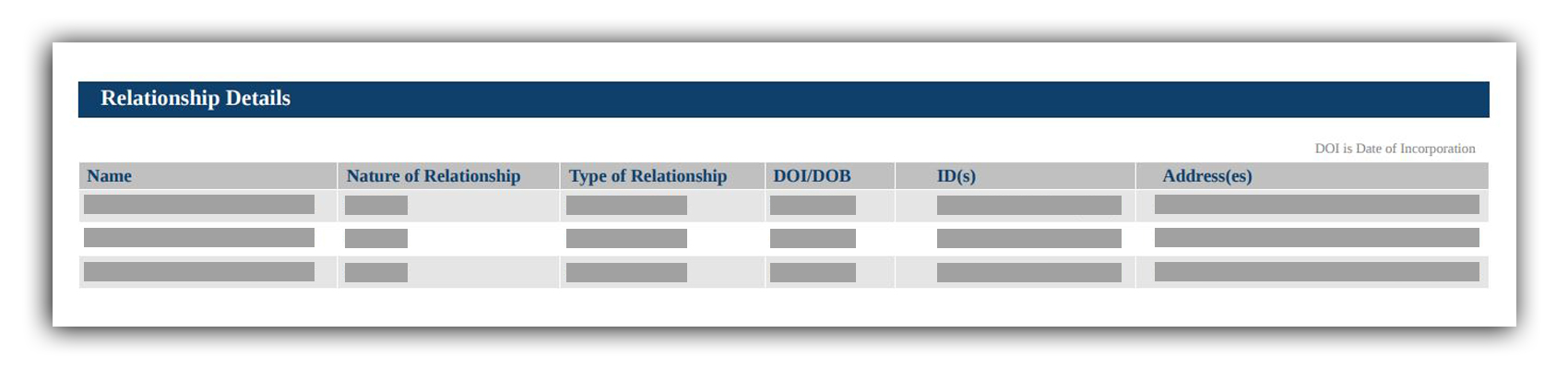

Relationship Details

This section outlines stakeholder relationships within the company, listing proprietors, partners, promoters, and other related entities.

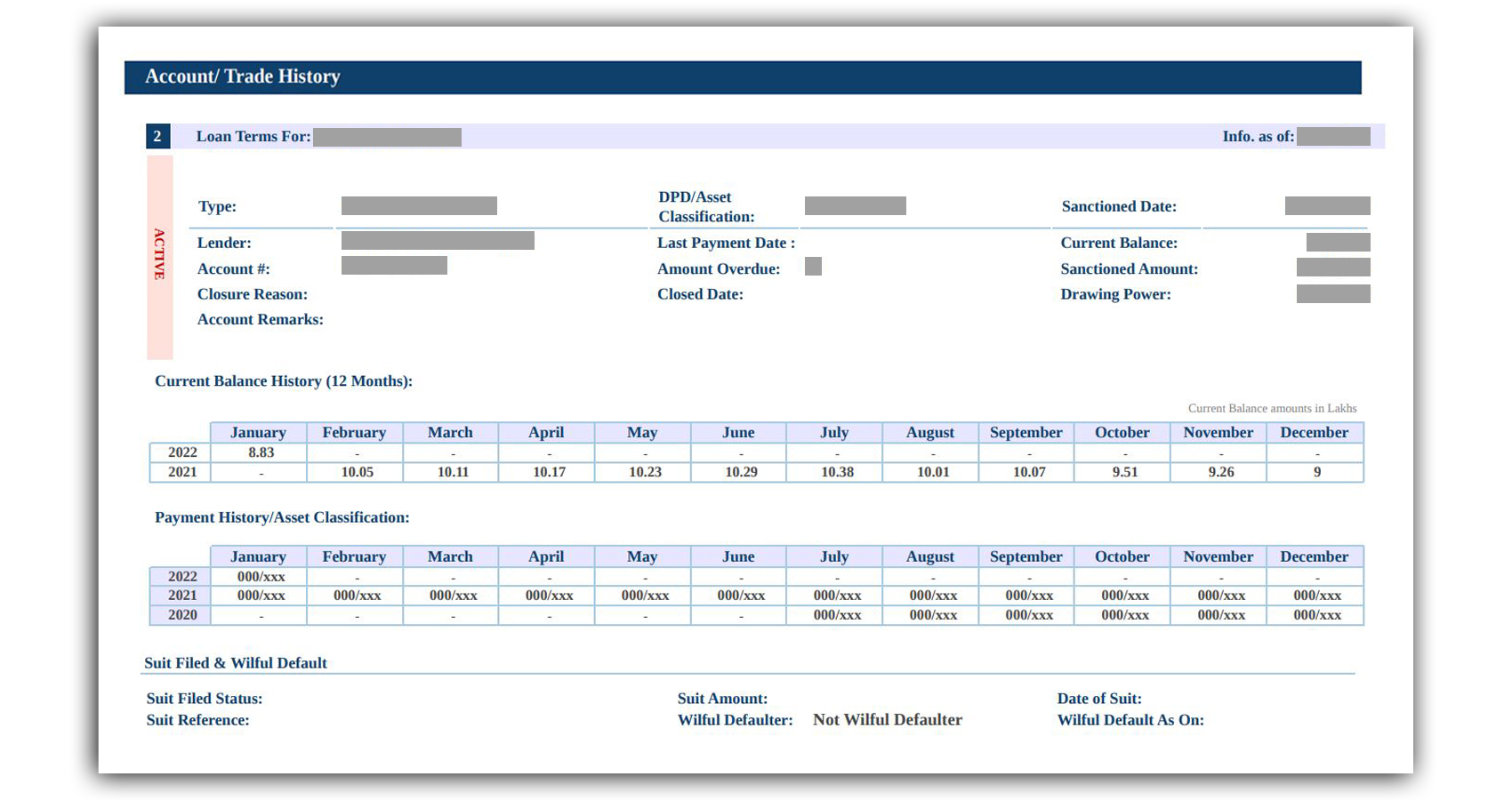

Account and Trade History

This section offers details about the different loans you have taken in the past (active and closed) and contains five sub-sections:

a) Loan Terms – Applicant as Borrower

This section gives an overview of loan terms, indicating whether loans are active or closed, along with lender details, loan types, sanctioned amounts, and current balances.

b) Current Balance History (Last 12 Months)

A month-wise record of outstanding loan balances over the past year is presented here.

c) Payment History and Asset Classification

This section highlights repayment behaviour and asset classification over the loan tenure, helping lenders assess payment discipline.

d) Suit Filed and Willful Default

Any suits filed against the business or instances of willful default are summarised in this section.

e) Guarantor Details

Details of guarantors, including name, PAN, address, and contact information, are listed here.

Inquiries Reported in the Last 24 Months

This section records all business credit inquiries made in the last 24 months, including the lender name, inquiry date, purpose, loan amount, and ownership type.

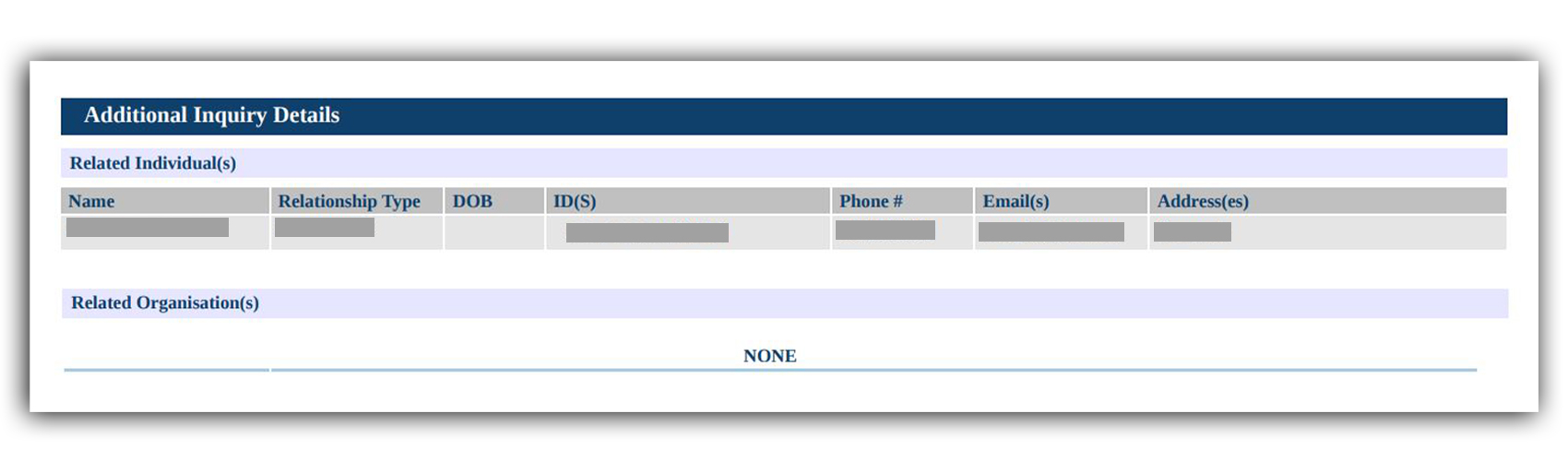

Additional Inquiry Details

Information about related individuals and associated organisations, such as parent, sister, or subsidiary companies, is included here.

Comments

Any additional remarks not covered in earlier sections appear here.

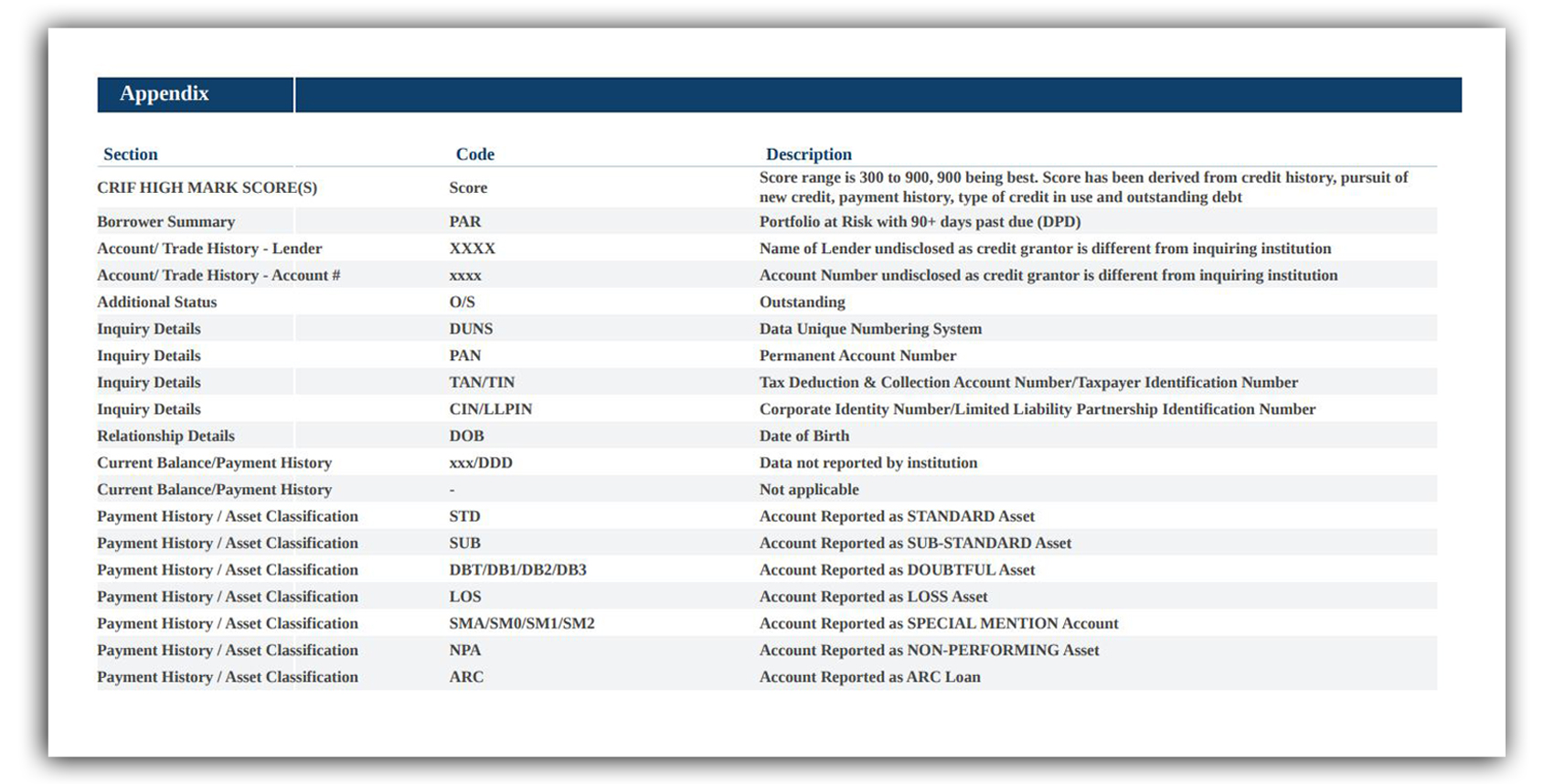

Appendix

The appendix explains all codes and abbreviations used in the report, enabling easier interpretation.

Why Understanding Your CRIF Company Credit Report Matters?

Your CRIF company credit report and score are powerful tools when applying for a business loan. They help lenders assess your creditworthiness while allowing you to identify gaps, address risk areas, and improve your credit profile. Once you understand how to read and interpret your report, you can use it strategically to strengthen your credit score and finance your business more effectively.

.