How & When to Dispute Your Credit Information Report?

Short Answer - Errors in a credit report can adversely affect your credit score and loan eligibility. Regularly reviewing your credit report and promptly disputing inaccuracies with supporting documents helps protect your financial profile, ensures accurate reporting, and restores credit health over time.

Errors in a credit report can significantly impact your credit score and reduce your chances of loan approval or access to new credit. Such inaccuracies may arise from data entry mistakes, lender errors, or even identity theft, making regular credit monitoring essential.

Understanding how credit reports work empowers you to identify discrepancies early and take corrective action. Once an error is detected, credit bureaus provide a structured dispute process that allows consumers to challenge incorrect information and restore the accuracy of their credit history.

How to File a Credit Dispute?

Filing a credit dispute is a formal process that allows you to correct inaccurate or outdated information in your credit report. Since credit decisions rely heavily on reported data, even minor errors can affect your creditworthiness. The steps below outline a clear, systematic way to raise a dispute, support it with documents, and track corrections to restore the accuracy of your credit history.

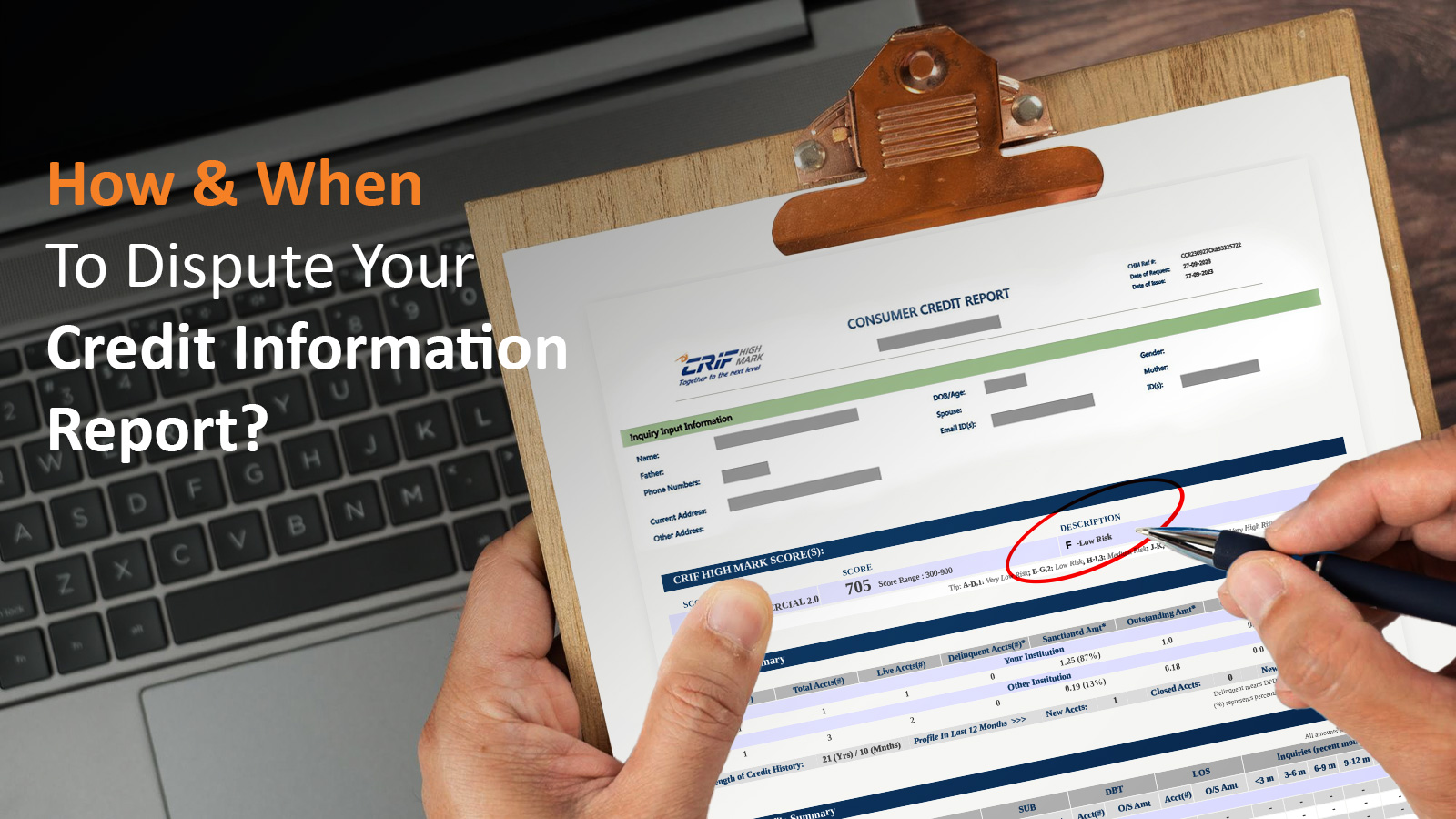

Step 1: Download your credit report

First off, you need to download the detailed credit information report from any of the credit bureaus in India, such as CRIF High Mark. You are entitled to download one free credit report each year.

Step 2: Inform the credit bureau

Once you are sure about the discrepancy in your report, you have to make it known to the 4 credit bureaus on their respective websites and postal addresses. This information has to be shared in the form of an online appeal and in writing via a letter. The letter should clearly contain each item in your report that you dispute. You need to state the facts and explain why you dispute the information and want it removed or rectified. The letter should be supported with copies of documents verifying your dispute. Always request a read receipt for your letters.

Step 3: Contact the Lenders

To ensure the errors are resolved at the source, it may also be a good idea to contact the lenders who supplied the incorrect information to the bureaus. Lenders, also known as furnishers, are the companies that provide the information to the credit bureaus. They include banks and credit card issuers. You can go to the furnisher and ask them to correct the mistake in case it is apparent that the mistake is rectifiable at their end. But if the error is an identity-related mistake made by a credit bureau, it may not be necessary to contact your lenders; you can contact the bureau directly.

Step 4: Count 30 days

The credit information companies are required to investigate your claim of dispute, which generally lasts at least 30 days. During this time, the item on your credit report that is under dispute will be temporarily removed from your credit report. After they have finished their investigation, the bureau is also required to provide you with a free copy of your credit report if it has now changed. While the process can be time-consuming, it is important to continue to dispute incorrect information on your report that negatively impacts your credit score. You can also ask the credit bureau to include information summarizing the dispute on your credit report so future lenders can see your claims and assess them for themselves.

Step 5: Check your credit report:

Updates to your affected credit reports may take some time to appear. It is dependent on the specific credit bureau’s update cycle and when the lender sends the new information to the credit bureau. If the update doesn’t appear on your credit reports within several months, contact the credit bureaus and the lender to verify that it’s reporting your account information to the bureaus.

What Should You Do After Disputing an Error on Your Credit Report?

Disputing inaccurate credit information is a crucial step toward safeguarding your creditworthiness. While the resolution process may take time, following up with credit bureaus and lenders ensures corrections are implemented accurately. Consistent monitoring helps prevent future errors and keeps your credit profile reliable for lenders.

.