Understanding CRIF Company Credit Report with Sample

Company credit report and score are the core elements defining your business’ creditworthiness and can impact your odds of getting a business loan. But what exactly is in your company credit report? The CRIF company credit report has information about your:

- Business: Information about your business, such as nature of business, industry, address and contact information, and stakeholders (partners, promoters, and holding company). It also includes a summary of any credit facilities you may have availed of in the past and their current status.

- Business credit score: The credit score informs potential lenders about your creditworthiness based on your repayment track record for past loans.

- Loan history: Information about every credit facility you have availed in the past, their current status, and repayment history (past 36 months) for active credit facilities. This also includes any credit facilities you have guaranteed as a business.

- Past searches: Details about all inquiries requested by a lender with CRIF against your company and the number of credit facilities you have sought out from new lenders over the last 24 months.

These are some of the important insights you can find in a business credit report. The CRIF company credit report is, however, much more detailed. Read on to know how you can read and interpret your CRIF business credit report and what each section of the credit report means.

How to Read and Interpret Your Business Credit Report?

To correctly read and interpret your business credit report, you need to first understand the different sections of the report and the information they contain. The most significant sections in your company credit report are:

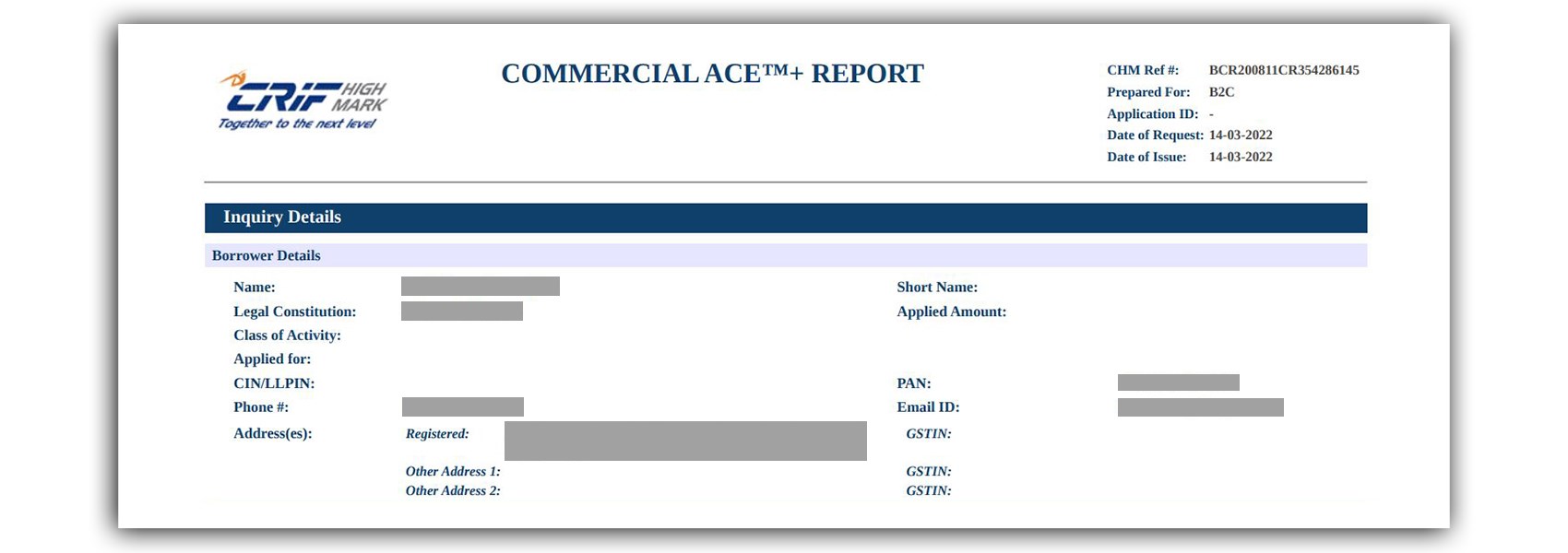

Inquiry Details

This section outlines your details as a borrower, including the name of your business, its legal constitution and class of activity, address and contact details, CIN, PAN, and GSTIN.

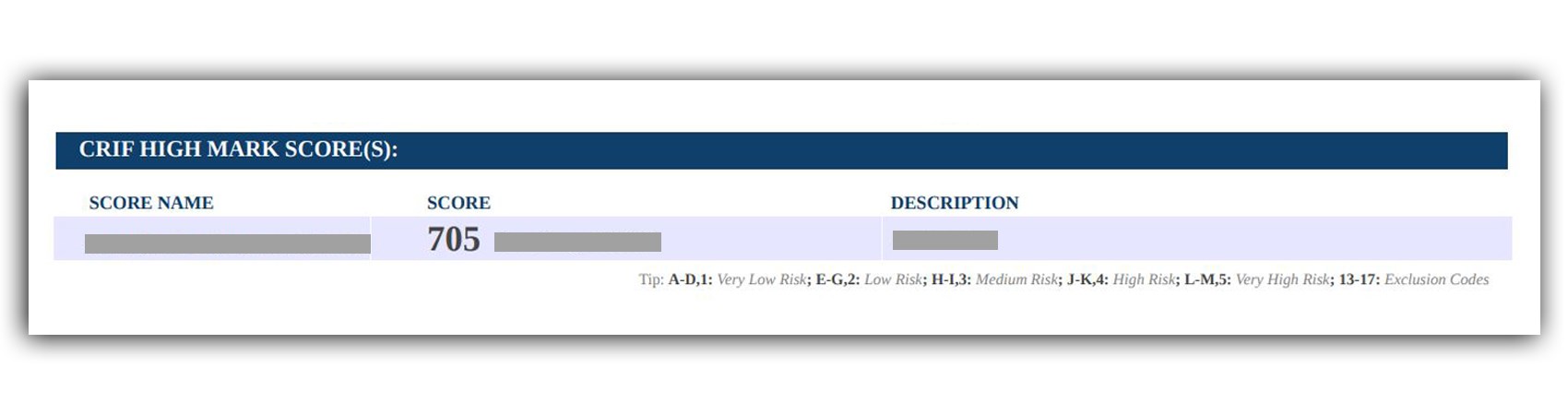

CRIF High Mark Score/s

This section highlights your company credit and credit risk, which will dictate your likelihood of loan approval. The score is depicted in the range 300 to 900 or as a rank from 1 to 5 depending on the exposure and number of tradelines.

Interpreting the Description:

- A-D: Very Low Risk

- E-G: Low Risk

- H-I: Medium Risk

- J-K: High Risk

- L-M: Very High Risk

- 13-17: Exclusion Codes

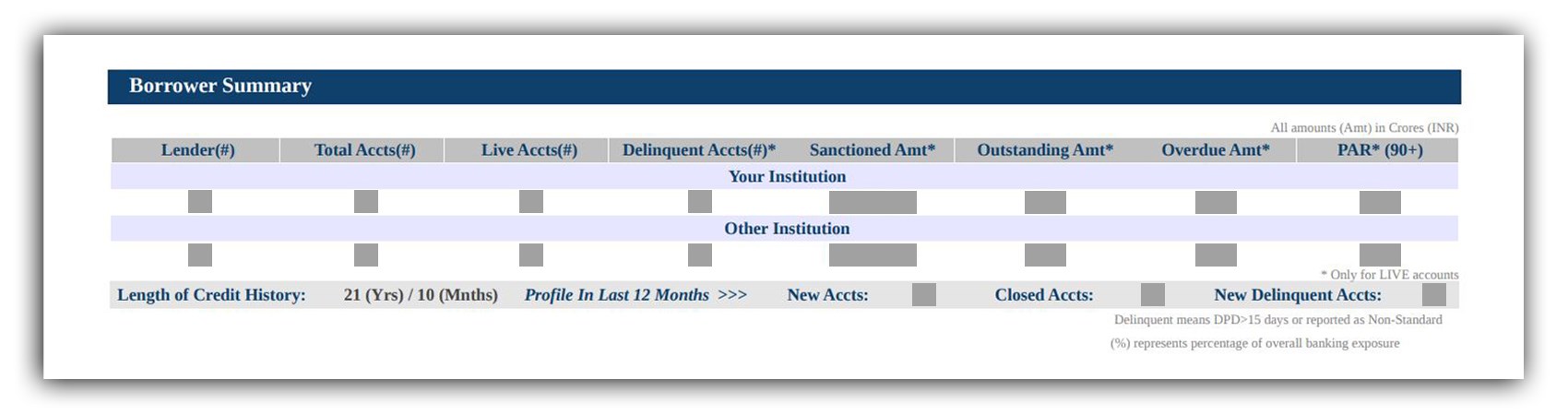

Borrower Summary

This section summarizes your credit history, including the number of your past lenders, the amount of loan, outstanding dues, and payment status (over the last 12 months) for you or the loans you have guaranteed.

*A delinquent account is a debt or loan that has not been paid on time and is now past due.

* PAR means Portfolio at Risk – Total Outstanding Amount of accounts with DPD > 90 days.

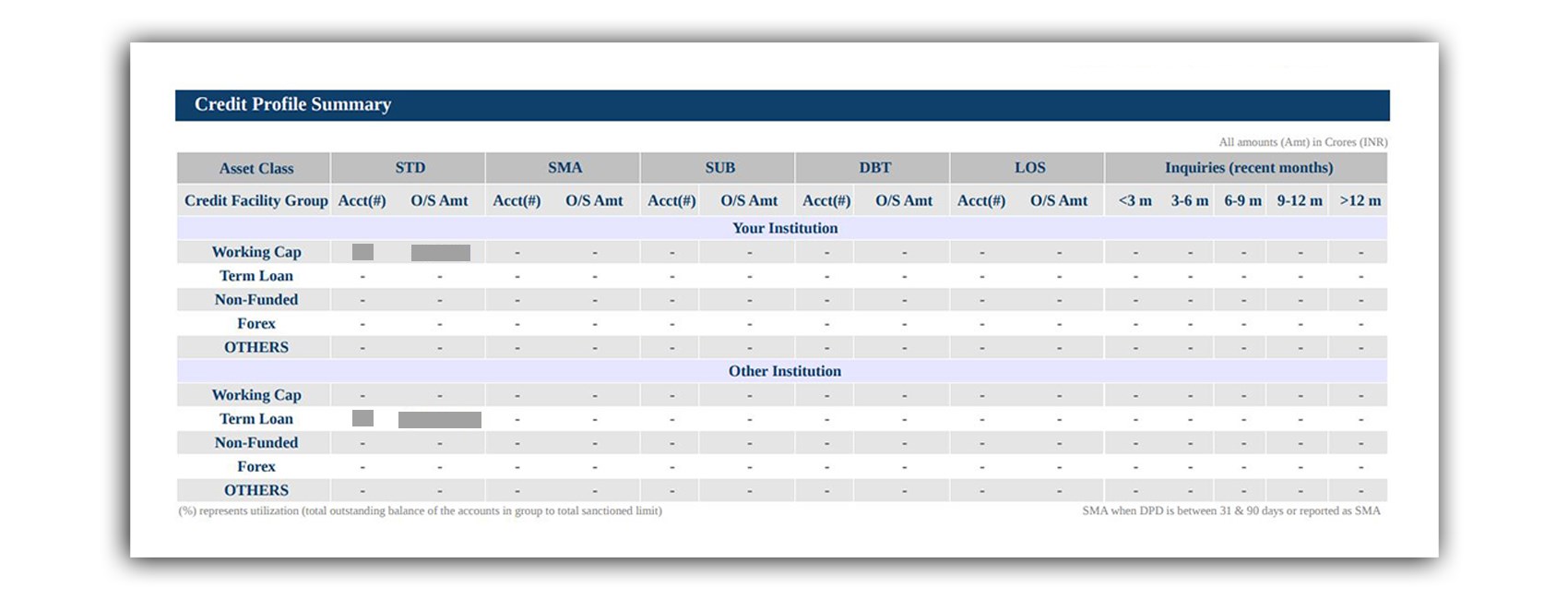

Credit Profile Summary

This section outlines your credit profile, including the type of loan, sanctioned amount, total outstanding amount, credit utilization, and credit inquiries in recent months for your business and the loans you have guaranteed.

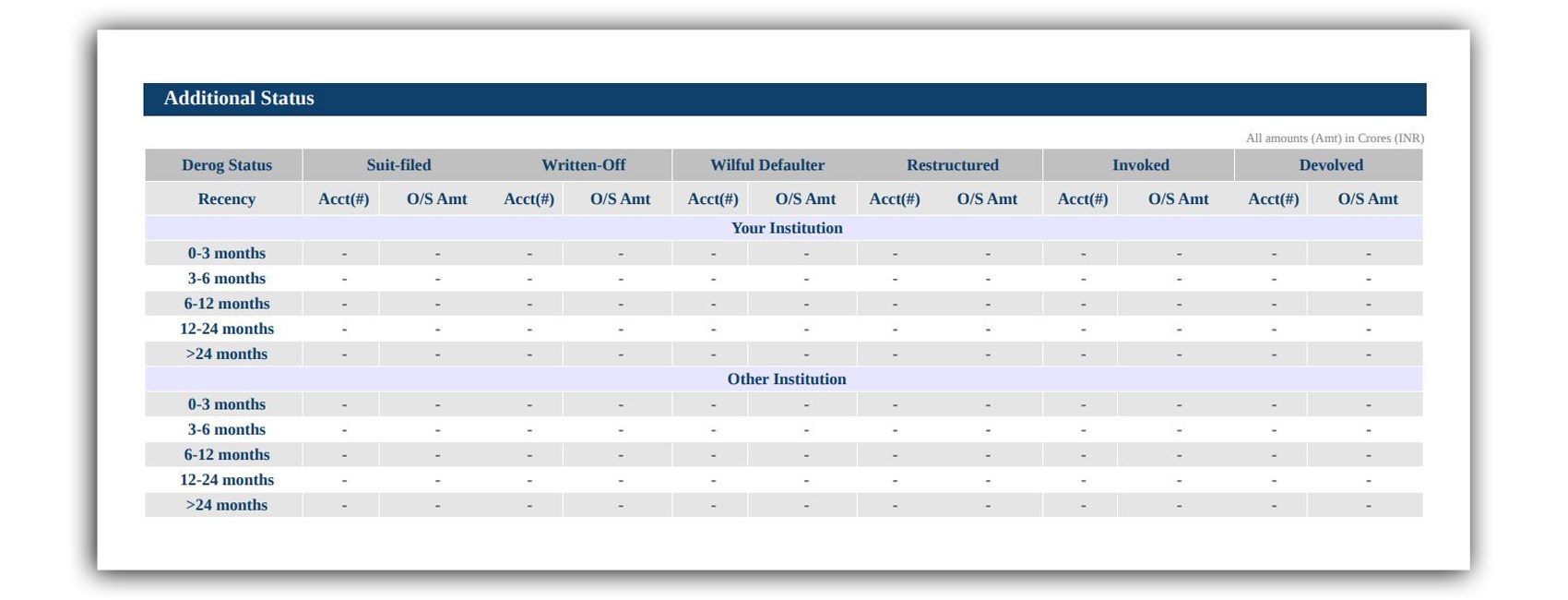

Additional Status

This section outlines the derogatory information about willful credit defaults or write-offs, suits files, credit facilities invoked or devolved, and restructured credit facilities over the last 2 years.

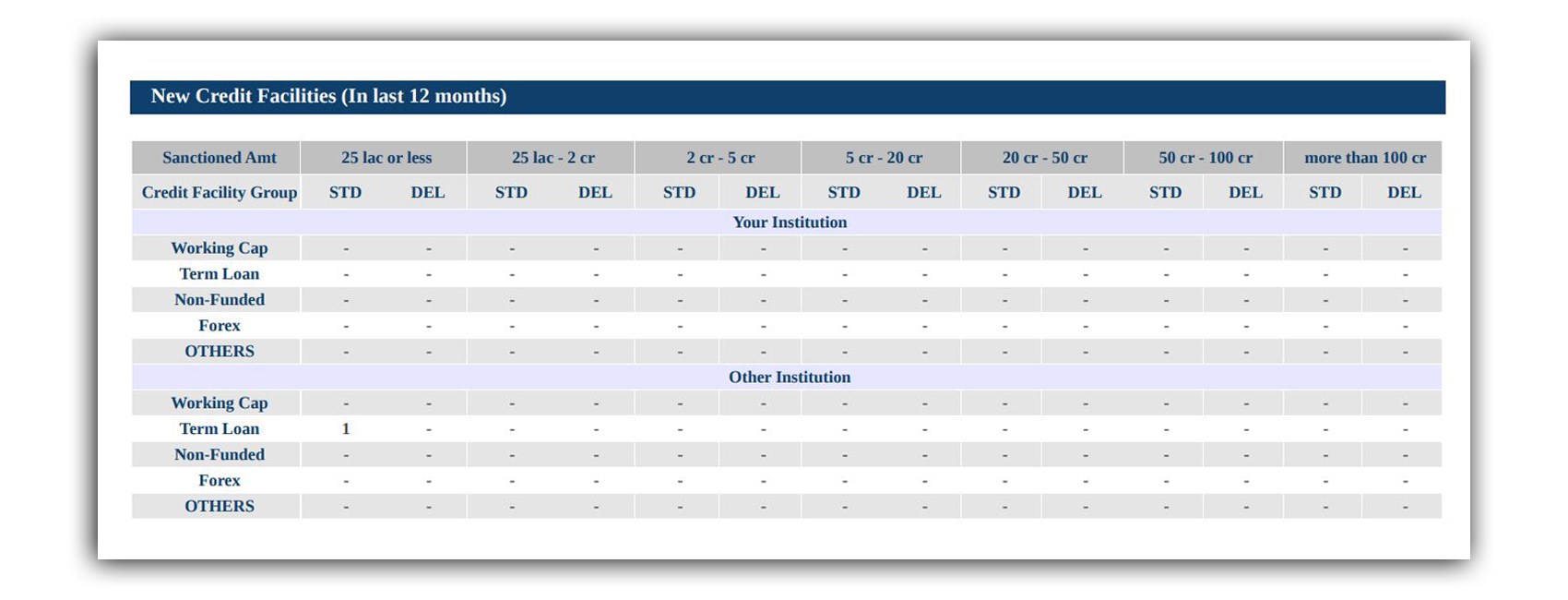

New Credit Facilities

Any new credit facility you have availed (working cap, term loan, or forex) in the last 12 months appears in this section.

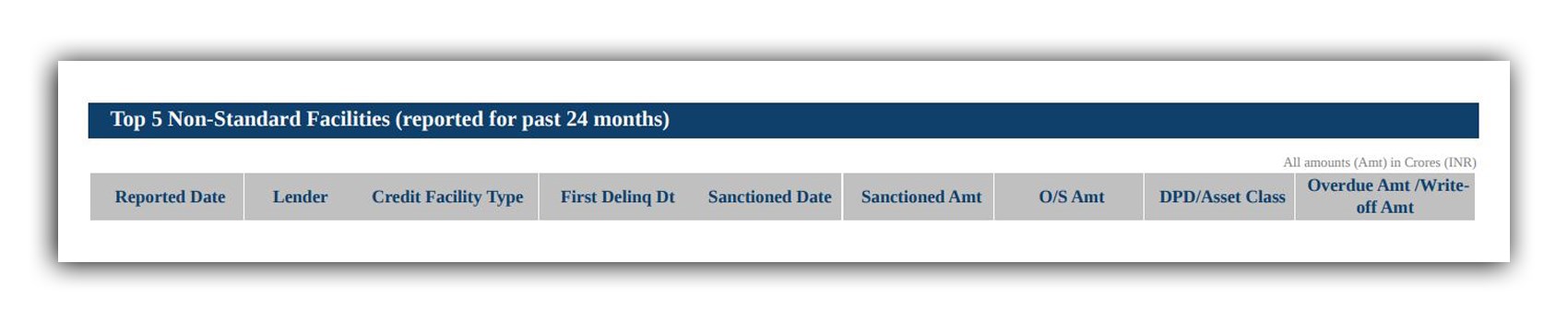

Top 5 Non-standard Facilities (reported for 24 months)

Any non-standard credit facilities you have availed in the last 24 months appear in this section. This contains information such as the lender’s name, credit facility type, sanction amount and date, outstanding amount, and overdue amount.

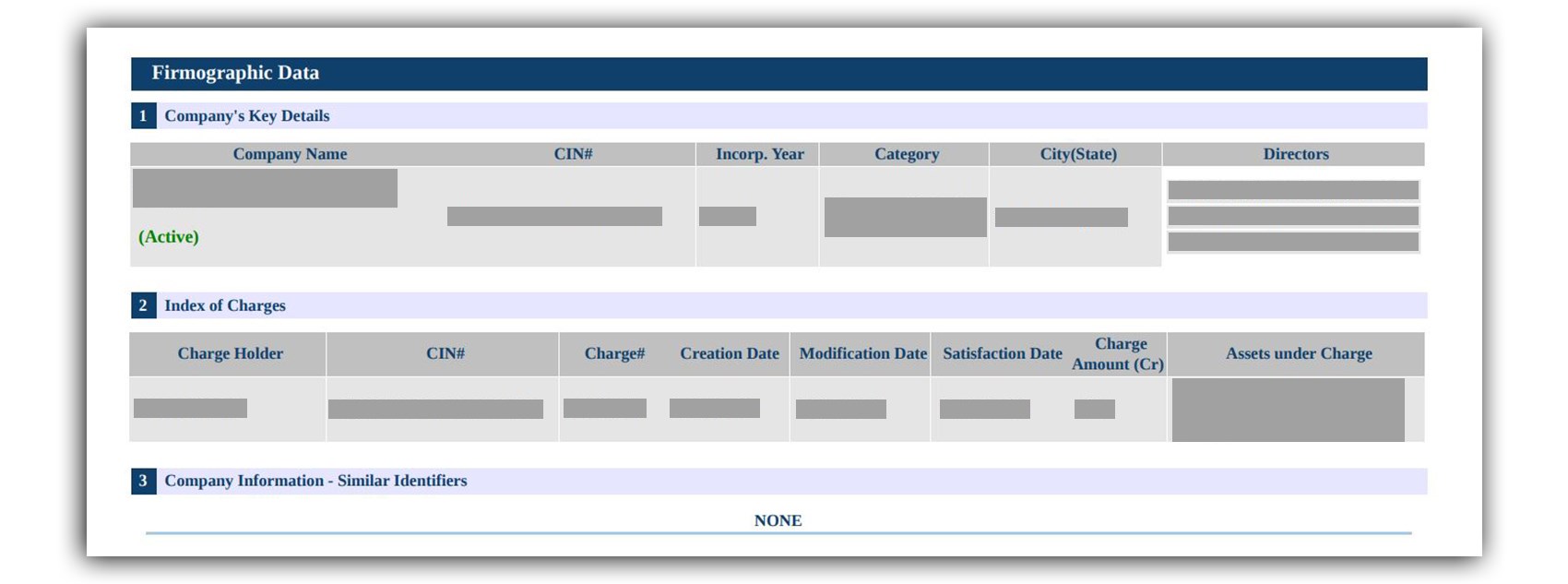

Firmographic Data

This section outlines the company information, including key company details, charges index, and other similar information to give lenders more details about your company as listed by the Ministry of Corporate Affairs (MCA).

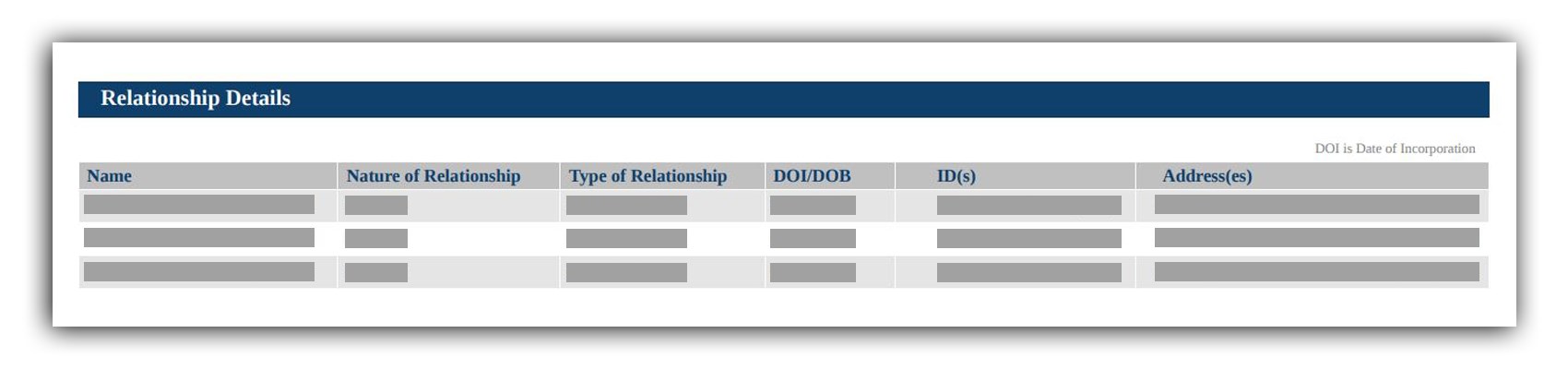

Relationship Details

This section outlines various stakeholder relationships within the company, listing proprietors or partners within the company.

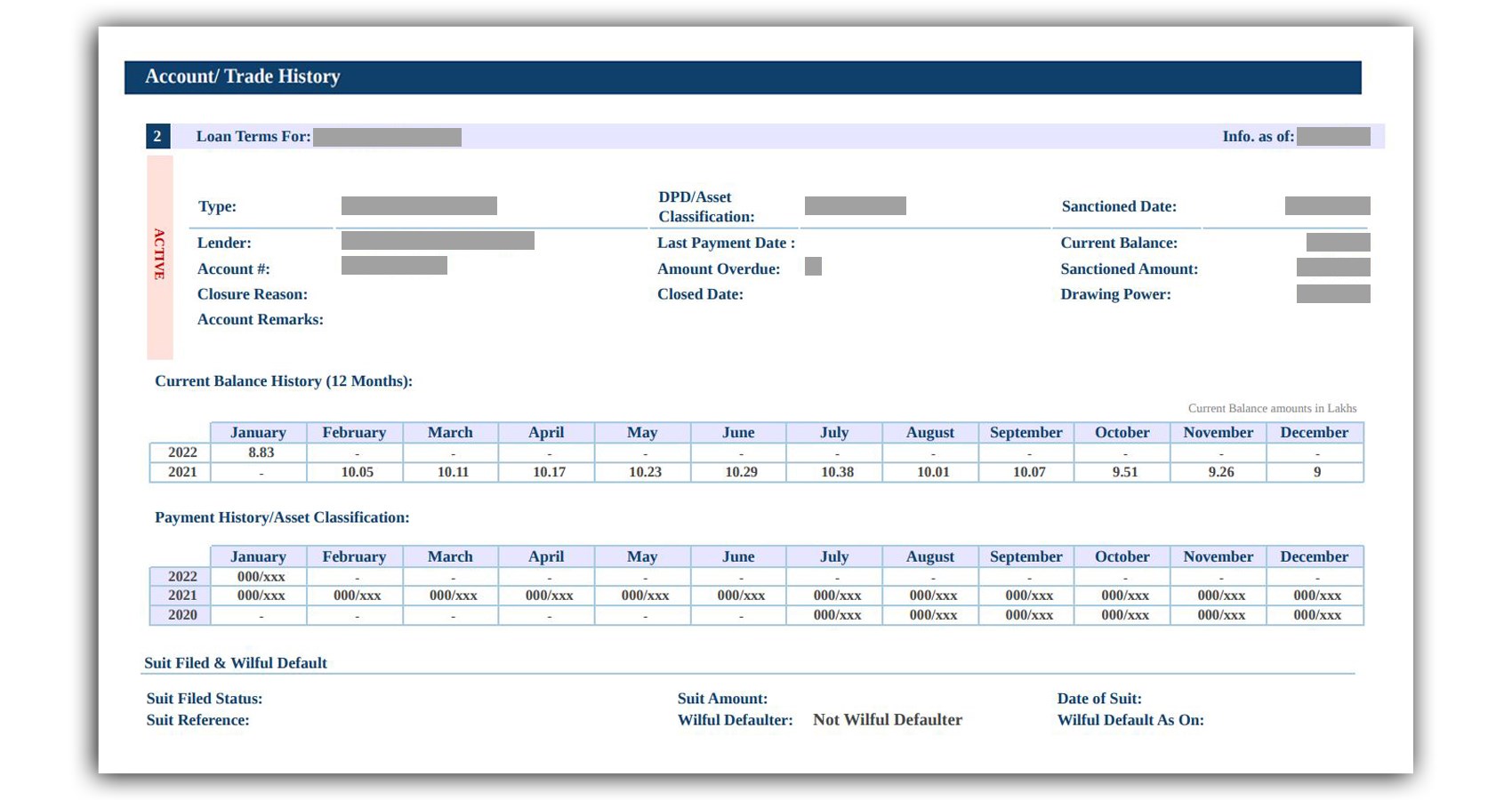

Account / Trade History

This section offers details about the different loans you have taken in the past (active and closed) and contains five sub-sections:

Loan Term For: Applicant as Borrower

This section gives a snapshot of the loan terms, specifying whether the loan is active or closed, who the lender is, the type of the loan, loan account details, sanctioned amount, and current balance.

Current Balance History (12 Months)

This section tabulates your outstanding loan balance over the last 12 months.

Payment History / Asset Classification

This section highlights your loan repayment history and indicates how you have classified your assets over the loan term.

Suit Filed and Willful Default

A summary of any suits filed against you or any willful default on your part appears in this section.

Guarantors

This section lists the details of guarantors, including name, PAN, contact details, and address, for your loan.

Inquiries (Reported for Past 24 Months)

The details of any business loan or credit report inquiry in the past 24 months will appear in this section. These include the entity that started the inquiry, the date and purpose of the inquiry, ownership type, loan amount, and any additional remarks.

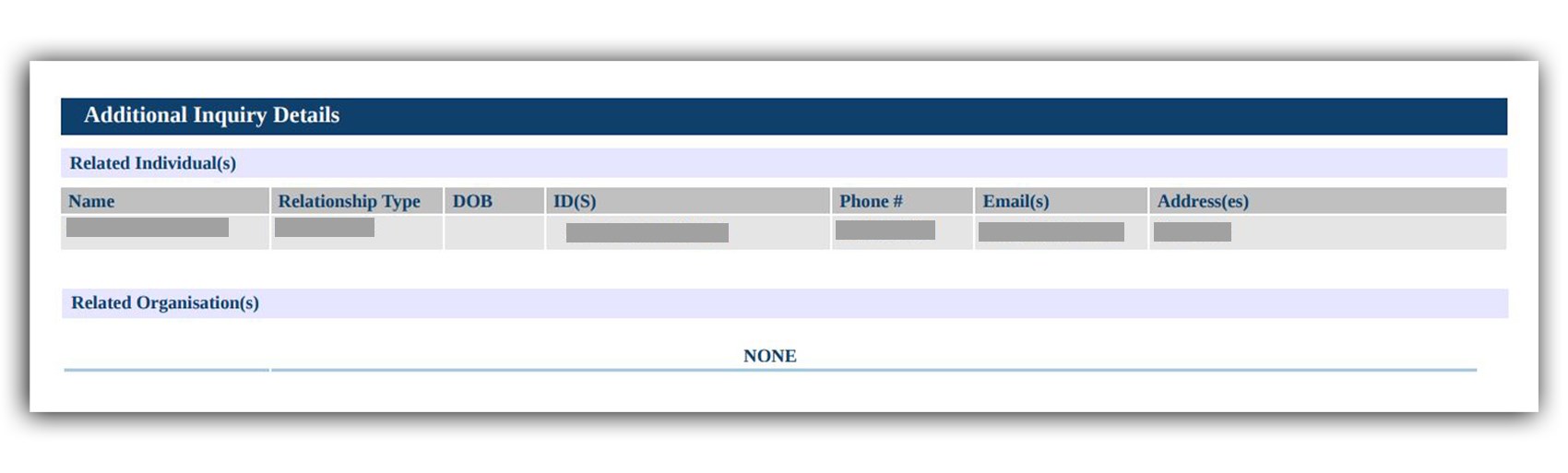

Additional Inquiry Details

This section lists all the related individuals (like proprietors or partners) and related organizations (parent, sister, or subsidiary organizations) of the borrower.

Comments

This section lists any additional comments – not pertaining to the previous sections – about the credit report.

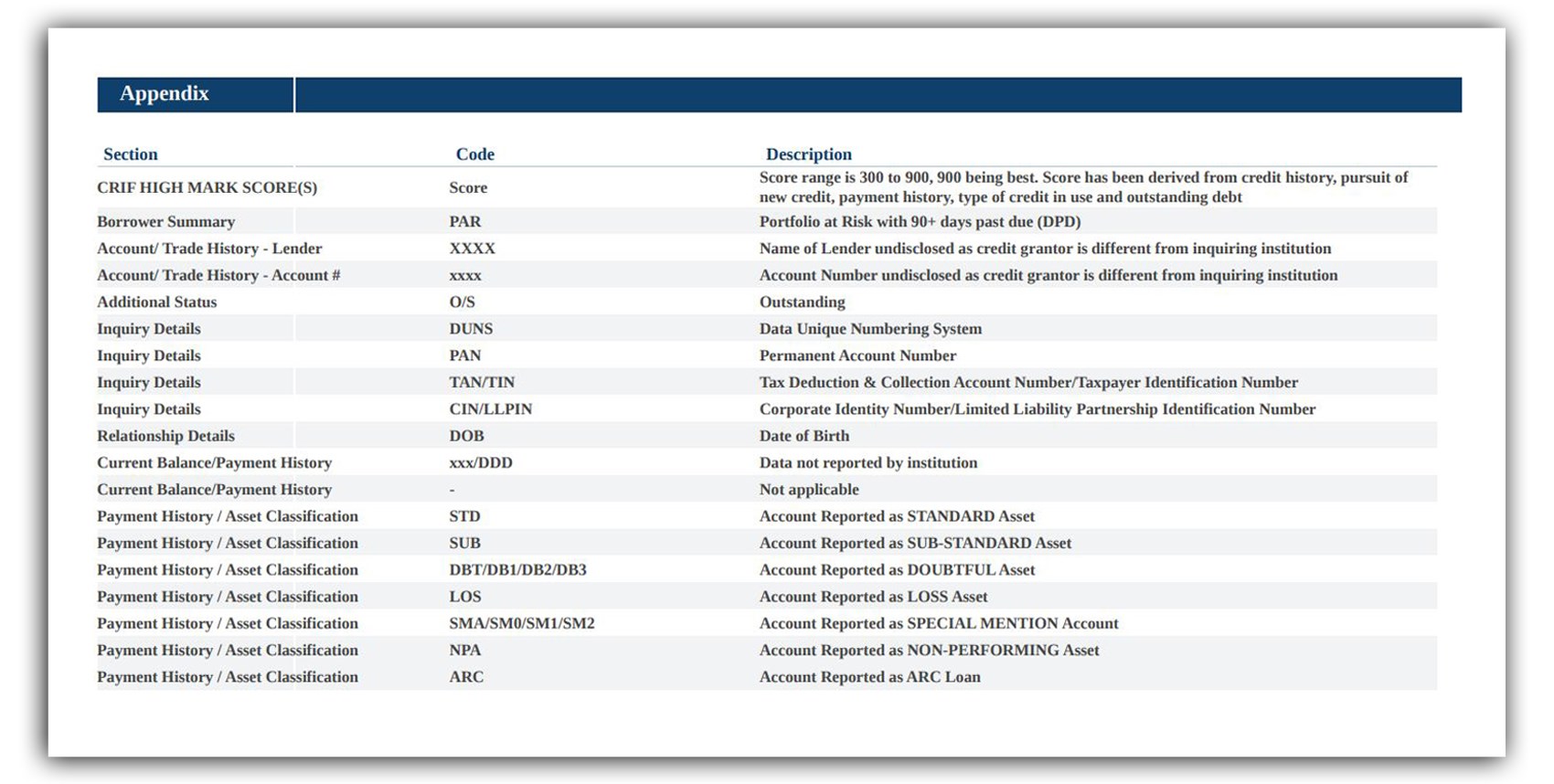

Appendix

The last section of the credit report lists and describes all the codes (or abbreviations) in the credit report so you can easily read and interpret your company credit report.

Your company credit report and score are great tools for you when applying for a business loan, giving the lenders an idea about your creditworthiness, and allowing you to identify any problem areas and improve your credit score. And once you know how to read, interpret, and understand your company credit report, you can use it effectively to build your credit score and use it to finance your business venture effectively.