How to get Business Loan in India? | CRIF High Mark

There are over 42.5 million registered and unregistered small and medium-sized businesses in India. Furthermore, the economy relies heavily on MSMEs to drive the country’s GDP growth. Undoubtedly, SMEs in India need capital investment backed by financial institutions and governmental entities to operate and grow. In FY21, loans to MSMEs in India totalled Rs. 9.5 trillion.

All these figures do show the burgeoning expansion of Indian business. However, you will want to know how to obtain a business loan if you intend to expand your current business or start a new one. We will go over various aspects of business loans in India in this guide, along with the steps you can take to ensure a smooth loan disbursement.

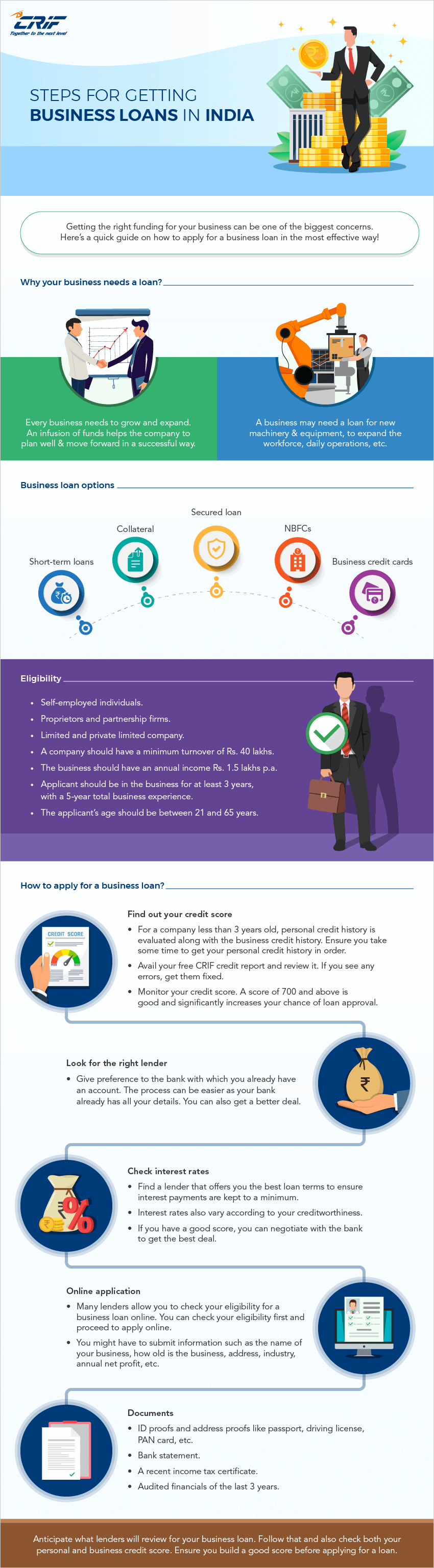

Why Does Your Business Need a Loan?

Businesses require loans for running the operations or further expansion into new lines of business through research & development.

The issue is that keeping track of all those expenses, on top of the overhead costs of running your business and spending upfront for your business needs, is possible as your business grows. It’s a vicious circle. You can’t grow unless you invest, but how can you invest while keeping money in the bank for operational expenses?

A small business loan could be the solution. While debt can be intimidating for small business owners, a loan can help you finance changes in your business that will result in a high return on investment.

Here are five reasons why your company might require a loan:

- The most obvious justification for considering a small business loan is investing in a business expansion Loans can assist you in covering the costs of growing your business without depleting your operational funds, allowing you to keep impressing clients while continuing to expand.

- Cash flow is always a dilemma for a small business, and it can become even more difficult when you have customers who don’t pay for services or unsold inventory that must be moved to bring in new products. A short-term loan can help your company survive lean times by giving you money to cover regular operating expenses.

- Once you’re up and running, you’ll need to keep growing and replenishing your stock to meet demand. You can stay ahead of the game and customer demand by taking out a loan to cover inventory costs without negatively impacting your cash flow.

- Unplanned costs like repairing or replacing broken equipment can destabilise your budget. With loans, you can keep your business current with cutting-edge technology that enhances your ability to serve customers and manage equipment maintenance costs.

- Obtaining a small, simple-to-repay loan before you require a larger one can help ensure that you receive favourable terms on the larger, more important loan. If you repay the small loan early, you can negotiate a better rate when you eventually need a larger loan.

Business Loan Options

Small-business loans come in various forms, each with advantages and disadvantages. Choosing the best one for your company will depend on when and for what purpose you need the money. A few types are:

- Term loan – Best for large businesses to cover the cost of investment in infrastructure, machinery, or R&D. Its tenure ranges from one to five years.

- Start-up loan – Covers the expenses of a start-up venture. Its tenure and interest rate depend on expected turnover and the time for which the business is running.

- Working capital loan – Working capital loans take care of seasonal crunches or demand spikes.

- Invoice financing – It is for small businesses to take care of the expenses between raising invoices and receiving payments. The bank disburses the loan against the invoices.

- Equipment financing – Manufacturing industries take this loan with the machinery as collateral.

- Loan against property – This loan can have the longest tenure, between 10 and 20 years and comes against the property as collateral.

Business Loan Eligibility Criteria

- Minimum turnover of Rs. 40 lakhs.

- Good Company Credit score

- The business should be running for a minimum of 3 years with a total experience of 5 years.

- Profit-making for the previous 2 years.

- Minimum annual income of Rs. 1.5 lakhs per annum.

- Applicant should be between 21 and 65 years of age at the time of loan maturity.

- Self-employed individuals, private limited companies, proprietors, and partnership firms can apply.

How to Apply for a Business Loan?

Plan your intended use of the funds and your expected return on investment. Once you have a strategy, follow the right procedure to get a business loan

Steps to getting a business loan

Find out your credit score

- Personal credit history is evaluated alongside business credit history for companies less than three years old. Try to get your personal credit score in order.

- Request your CRIF Business credit score report. If you notice any errors, please fix them.

- Keep track of your credit score. A credit score of 700 or higher is considered good and significantly increases your chances of loan approval.

Look for the right lender

- Preference should be given to the bank with which you already have an account. The process could be simplified, and your bank already has all your information. You can also negotiate a better price.

Check interest rates

- Find a lender who will give you the best loan terms to keep your interest payments to a minimum.

- Interest rates are also affected by your creditworthiness. You can negotiate with the bank to get the best deal if you have a high credit score.

Online application

- You can check online to see if you qualify for a business loan from a lender. You can negotiate with the bank to get the best deal if you have a high credit score.

- You might be required to provide details about your company, including its name, years of operation, address, industry, net profit per year, etc.

Documents

- ID proof and address proof like passport, driving license, PAN card, etc.

- Bank statement

- Recent Income Tax certificate

- Audited financials for the last 3 years

Every business is unique. The business plan, loan requirement reason, tenure, and interest rate may differ. Evaluate the terms and conditions of different lenders and choose the one that provides the best deal with a smooth application process.